The SEC issued a Proposed Rule (PDF - 1.88KB) (PDF - 2.1MB), ( The Enhancement and Standardization of Climate-Related Disclosures for Investors, which would require all registrants to include certain climate-related information in registration statements and periodic reports.

The climate-related disclosure framework in the proposed rule is modeled after the Task Force on Climate-Related Financial Disclosure’s (TCFD’s) recommendations, as well as the Greenhouse Gas (GHG) Protocol, which is a commonly accepted standard. The proposal is intended to address investors’ needs and to help registrants disclose climate-related risks more efficiently and effectively.

The proposed amendments would strengthen the existing disclosure requirements, including the SEC’s 2010 climate-related interpretive guidance (PDF - 1.88KB) (PDF - 145KB). Drawing from this guidance, the SEC’s Division of Corporation Finance (CorpFin) recently released a sample letter illustrating comments that CorpFin staff might issue to companies related to climate-related disclosures or the absence of such disclosures.

The proposal’s comment period ends on the later of 30 days after it is published in the Federal Register or May 20.

Regulation S-K

The proposed amendments would add new subpart 1500 to Regulation S-K, which would require qualitative disclosures on climate-related risks, governance and risk management, and impacts on a registrant’s strategy, business model, and outlook in addition to quantitative GHG emissions metrics.

The proposed disclosures would be required in registration statements and in periodic reports, such as in Form 10-K, and would be required to either be presented in a separate, appropriately captioned section or be incorporated by reference from another section of the document or from other filed or submitted reports.

Governance and risk management

Proposed Item 1501 would require a registrant to disclose certain information about its board of directors’ oversight and management’s governance of climate-related risks.

The board oversight disclosures would include

- Identification of any members or committees responsible for the oversight of climate-related risks and the frequency by which they meet to discuss the risks

- Identification of any member that has expertise in climate-related risks and the nature of the expertise

- How climate-related risks are considered as part of the registrant’s business strategy, risk management, and financial oversight

- Whether and how climate-related targets or goals are set and how progress is measured

The management governance disclosures would require a registrant to disclose management’s role in assessing and managing climate-related risks. The requirements would include disclosures similar to those noted in the preceding bullets for board oversight, as well as disclosures on how often the management committee reports climate-related risks to the board.

Proposed Item 1503 would require a registrant to disclose the processes that a registrant uses to identify, assess, and manage climate-related risks. If a registrant has a separate board or management committee that is responsible for assessing and managing climate-related risks, the registrant would be required to disclose how that committee interacts with the board or management committee governing risks.

Lasty, if a registrant uses insurance or other financial products to manage its climate-related risks, it may be required to disclose the use of these products if, for example, the extent of loss of insurance coverage or increase in premiums is reasonably likely to have a material impact on the registrant’s business.

Strategy, business model, and outlook

Proposed Item 1502 would require a registrant to disclose whether any climate-related risks are reasonably likely to have a material impact on the registrant’s business or consolidated financial statements that might occur in the short, medium, and long term. The registrant would be required to define those time horizons as well as discuss its assessment of the materiality of climate-related risks over time.

A registrant would be required to specify whether the identified risks are “physical” or “transition” risks, as defined below, as well as the nature of the risks presented. Additionally, a registrant would be required to provide a narrative discussion of whether and how the risks have affected, or are reasonably likely to affect, the consolidated financial statements.

The proposal defines “physical risks” as acute and chronic risks to the registrant’s business operations or the operations of those with whom it does business. “Transition risks” refer to the actual or potential negative impacts on a registrant’s consolidated financial statements, business operations, or value chains attributable to regulatory, technological, and market changes designed to address the mitigation of, or adaptation to, climate-related risks, such as the transition to less carbon-intensive products.

A registrant would also be required to disclose the actual and potential impacts on its strategy, business model, and outlook, including the impacts on business operations, products or services, suppliers or others in the value chain, activities to mitigate the risks, expenditures for research and development, and any other significant impacts.

Item 1502 would also require a registrant to describe the resilience of its business strategy and any tool, such as scenario analysis, that it uses to assess the impact of climate-related risks on its business and consolidated financial statements.

Targets and goals

The disclosure requirements in proposed Item 1506 would be required if a registrant has set any targets or goals related to the reduction of GHG emissions or any other climate-related target or goal. The disclosures would include a description of (1) the scope of activities and emissions included in the target, (2) the unit of measurement, (3) defined time horizon of when the target may be achieved, (4) defined baseline time period and baseline emissions for progress tracking, (5) interim targets, and (6) how the registrant intends to meet its targets or goals.

Further, a registrant would be required to disclose more details regarding its use of carbon offsets or of renewable energy credits or certificates if they are included in a registrant’s plan to achieve its targets or goals.

Greenhouse gas emissions data

Proposed Item 1504 would require a registrant to report GHG emissions for the most recent fiscal year, and the historical periods included in the financial statements. A registrant would not be required to provide GHG emissions metrics for periods prior to the current reporting period if (1) it was not previously required to and had not presented its GHG emissions for those periods, and (2) the data is not reasonably available.

The required disclosure is based on the GHG Protocol. The proposal includes a variety of definitions to help registrants understand terminology and concepts pertinent to the identification and inventory of GHG emissions sources.

Emissions metrics

The proposal would require disclosure of GHG emissions in two ways: (1) disaggregated by constituent greenhouse gas, and (2) expressed in aggregate as CO2e, or carbon dioxide equivalent. Disclosed emissions would exclude the impact of any purchased or generated offsets.

Disclosed emissions are categorized as follows:

- Scope 1: direct GHG emissions from operations owned or controlled by the registrant

- Scope 2: indirect GHG emissions from the generation of purchased or acquired electricity, steam, heat, or cooling consumed by operations owned or controlled by the registrant

- Scope 3: all indirect GHG emissions not otherwise included in Scope 2 emissions, which occur in upstream and downstream activities of the registrant’s value chain, such as purchased goods and services or the use of the registrant’s products by customers.

A registrant, other than a smaller reporting company (SRC), would be required to disclose Scope 3 emissions if material or if the registrant has set an emissions reduction goal that includes Scope 3. The proposal also includes a safe harbor from certain legal liability for Scope 3 emissions disclosure.

A registrant would also be required to disclose intensity metrics regarding GHG in terms of metric tons of CO2e per unit of total revenue and per unit of production.

Grant Thornton insight:

Public and private companies alike continue to face ESG information requests and pressure from investors, customers, and other stakeholders for climate-related information, particularly regarding GHG emissions reported using the GHG Protocol. Whatever the outcome and timing of future SEC activity, these pressures are not expected to dissipate.

Many investors have also indicated a preference for the voluntary disclosure framework of the TCFD. Given that the SEC’s proposal is consistent with both the GHG Protocol and the TCFD, we believe that efforts to implement such disclosures in advance of regulated disclosures would greatly reduce implementation efforts related to any SEC requirements.

In addition, boards, directors, and management of public and private companies may have significant changes ahead of them to identify and mitigate climate-related risks and opportunities. Many of the proposed disclosures may be helpful points for registrants to consider when developing their plans.

Methodology and related assumptions

The proposal would also require disclosure of the following items:

- Methodology, significant inputs, and significant assumptions used to calculate GHG emissions

- Organizational and operational boundaries used in calculating Scope 1 and Scope 2 emissions, which must be consistent with the scope of entities, operations, and assets applied in the consolidated financial statements

- Calculation approach and tools

- Use of third-party data, including the source, regardless of the applicable emissions scope

- To the extent material, any changes in methodology or assumptions from the prior fiscal year

- Any gaps in the data required to calculate emissions

Attestation

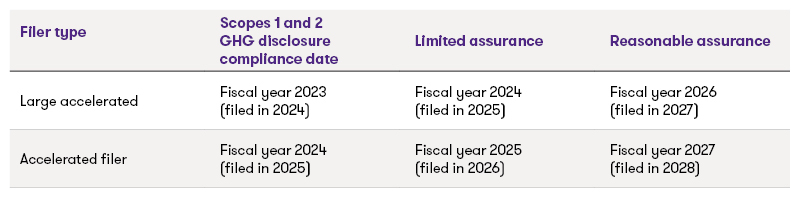

Scope 1 and Scope 2 emissions reported by large accelerated and accelerated filers are subject to phased-in assurance by a GHG emissions attestation provider. Limited assurance would be required beginning with the second reporting period, with a transition to reasonable assurance two years later. See the compliance dates section below for further details.

Regulation S-X

The proposed amendments would add new Article 14, Climate-related disclosure, to Regulation S-X, which would require a registrant to disclose, for each of the years presented in the financial statements, climate-related financial metrics as well as a discussion of certain estimates and assumptions underlying the preparation of the consolidated financial statements.

A registrant would also be required to disclose contextual information explaining significant assumptions, inputs, and policy decisions related to each metric.

Financial impact metrics

The proposal would require disclosure by financial statement line item of the positive and negative impact of the following:

- Severe weather events and other natural conditions. Examples noted include changes to revenue or cost from business or supply chain disruptions, impairment charges, or changes to loss contingencies or reserves from weather exposure.

- Transition activities, such as changes to revenue or cost due to new emissions regulations, cash flow impacts related to changes in upstream costs, a reduction in the carrying amount of assets due to reduced salvage value or estimated useful life, or changes to interest expense due to climate-linked bonds

Expenditure metrics

In addition, a registrant would disclose the aggregate expense and cost capitalized related to

- Efforts to mitigate risks of severe weather events and other natural conditions. A registrant that has disclosed GHG emissions reduction targets or similar commitments must also disclose the related expense or cost, if any.

- Actions to reduce GHG emissions or transition risks, for example, the cost to research new technologies, purchase energy credits, or improve energy efficiency

Financial estimates and assumptions

Under the proposal, a registrant would be required to indicate, in the notes to the audited financial statements, whether estimates and assumptions used to produce the consolidated financial statements were affected by risks, uncertainties, or known impacts from (1) severe weather or other natural conditions, and (2) the transition to a lower carbon economy or the registrant’s climate-related targets. If a registrant is affected by either (1) or (2), a qualitative discussion of the estimate would be required.

Impact of identified risks and opportunities

A registrant must disclose the actual impact to the above-described financial statement metrics or estimates from any identified physical and transition risks. In addition, a registrant is permitted but not required to disclose the impacts of climate-related opportunities to the above-described financial statement metrics or estimates; however, if provided, such disclosure would be required for all fiscal years presented and must be consistently applied across all financial statement line-items and identified opportunities.

Compliance dates

The proposed rule includes phased-in compliance dates to accommodate smaller registrants. The tables below, reproduced from the SEC’s Fact Sheet (PDF - 1.88KB) (PDF - 284KB), provide a summary, assuming the proposed rule is adopted as final in December 2022 and the registrant has a December 31 fiscal year-end.

Contacts:

Managing Director, ESG & Sustainability Services

Grant Thornton US

Marjorie is a Managing Director in the SEC Regulatory Matters Group, with more than 15 years of experience in auditing, accounting and SEC reporting.

Arlington, Virginia

National Managing Partner of Professional Practice, Audit Services

Partner, Audit Services, Grant Thornton LLP

Partner, Grant Thornton Advisors LLC

Kendra Decker is the national managing partner of Grant Thornton LLP’s Professional Practice within the firm’s Audit Quality and Risk group.

This Grant Thornton LLP content provides information and comments on current issues and developments. It is not a comprehensive analysis of the subject matter covered. It is not, and should not be construed as, accounting, legal, tax, or professional advice provided by Grant Thornton LLP. All relevant facts and circumstances, including the pertinent authoritative literature, need to be considered to arrive at conclusions that comply with matters addressed in this content.

For additional information on topics covered in this content, contact a Grant Thornton LLP professional.

Trending topics

Share with your network

Share