How directors can get maximum value from the audit

Audit innovations are continually advancing and should deliver insights beyond a higher quality and more efficient audit. Does your board know which innovations are being used on your engagement, why these technologies were chosen, and how the results are benefitting your company?

Too often, we fall in love with buzz words like data analytics, automation and AI. If it is new and shiny, it must be good. But are all the futuristic innovations on your auditor’s website right for your company? Are they really being used, and can they actually deliver insights such as operational improvements and peer benchmarking? This article will help directors identify what to ask.

The use of advanced technology on an audit engagement should be your baseline expectation of your auditor. A data-driven risk assessment offered through analytic tools can generate improvements to quality and effectiveness, and greater audit efficiency translates into time saved for your company that can be invested elsewhere. But we must not ignore an essential product and, in many cases, byproduct of audit innovation — insights. As we explore insights, it’s helpful to classify them into two principal categories, micro insights and macro insights.

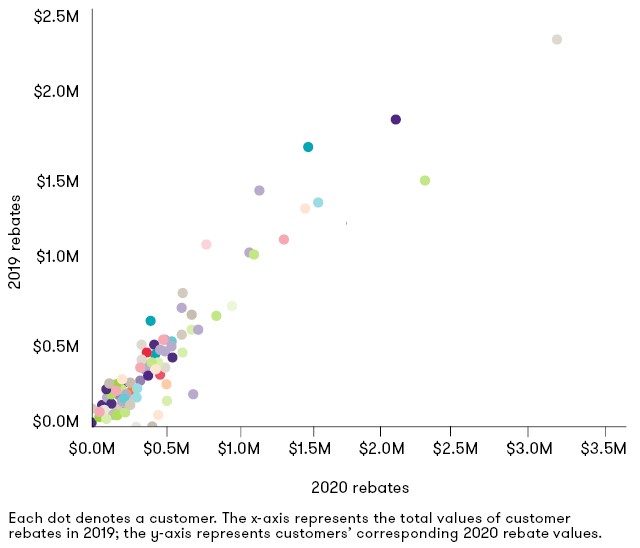

Micro insights are derived from transactional or other entity-level analyses. Examples include improved financial reporting risk assessment through the identification of “notable” transactions or classes of accounts, opportunities to accelerate the financial close process, or even optimize sales initiatives. Consider this rebates regression analysis performed in a recent engagement:

While this trend analysis was used in the audit to understand and test rebate activity, the auditors were able to identify certain customer behaviors not previously apparent to management. Equipped with these insights, the company began refocusing the rebate program to exclude customers who weren’t taking advantage of rebates. It also was able to reduce liabilities related to the program, clean up its balance sheet and increase working capital.

Macro insights apply more broadly at the industry or market level and leverage industry or sector perspectives, external data sources and the audit team’s experience. These insights are typically related to business performance or key performance indicators (KPIs) and may complement micro insights generated from the audit.

An example of a macro insight related to operational performance might be recognizing that a company’s sales per square foot are significantly below that of the company’s peer group; optimizing retail space could lead to significant growth in top-line revenue, gross margin and enterprise valuation.

Five questions for boards to ask

For the board to best understand how the auditor is using innovation to generate insights valuable to your company, here are five key questions to discuss with management and your auditor:

1. What innovations are being used in the audit and why?

Not all innovations are a fit for all companies. Expect your auditor to tailor the suite of available technologies for your industry and your company. For example, analyzing 100% of transactions may make little sense for businesses with very few lines of general ledger data, but it can be very meaningful for companies with a high volume of general ledger transactions, business segments or locations.

A revenue volatility analytic would better suit companies with consistent customer billings at regular intervals (e.g., software licenses or subscriptions) rather than a retail company with a range of sales to a variety of customers. In other cases, a revenue analytic might not be a fit at all.

Conversely, if there are innovations that would be accretive to the audit that are not being used, the board will want to understand the reasons for this and help to address any impediments to adoption resulting from the company’s financial reporting process, such as disparate incompatible IT systems.

2. How is audit innovation impacting the quality of the audit?

Analytics are improving quality by accurately pinpointing risk and narrowing auditors’ attention to those areas that require it. For example, revenue analytics enable the auditor to detect riskier transactions while spending less time on items that follow an expected pattern of behavior. What might your company learn about transactions deemed to be notable?

Automations are also improving the quality of the audit where teams are no longer manually compiling information. This might entail preparing and rolling forward workpapers, performing schedule analysis or even producing computations, such as an accounts payable turnover ratio or invoice aging in an accounts receivable subledger. When the auditor automates these important but tedious tasks, the team can focus on higher value activities that enhance overall quality.

3. How are innovations delivering efficiencies in the audit?

One of the goals of audit innovation is to create greater efficiency across the entire audit process, including for your people. Some efficiencies will be quickly realized and more obvious. For example, data analytics has reduced sample sizes by up to 50% when the data-driven insights revealed by analytics identify notable transactions that pose the greatest risk and help focus the audit team’s efforts. This means your company spends less time addressing auditors’ testing needs. And the auditor’s risk assessment can provide valuable insights regarding outsized risk in certain financial reporting processes or transaction streams.

Other innovation outputs will streamline processes and, over time, reduce friction in the audit approach. For these less obvious impacts, your auditor should be able to show you a baseline comparison over a few years as the technologies bring efficiencies to life. Audit firms must continually reinvest in their innovation, and many innovations require an initial level of effort to implement, so be wary of claims that every innovation will immediately reduce costs.

4. What audit insights can improve your financial performance?

Micro insights might include observations about financial performance that can streamline and enhance business processes. For example, analytics can spot repetitive manual entries that can be automated, or regression analyses could allow management to more accurately and rapidly develop estimates. Management will also need to consider how best to redeploy resources that are freed up due to efficiency opportunities identified by the auditors.

5. What audit insights can improve your reporting process?

At a macro level, the auditor’s understanding of peer companies in your industry should help provide perspective on how the company is performing relative to peers. Reviewing the results of analytics covering other companies in the same industry could reveal opportunities to improve certain financial ratios or KPIs.

It’s more important than ever to understand what innovations are being brought to bear and what insights the audit is generating that can help streamline your company’s financial reporting processes and improve operating performance. Don’t hesitate to ask about innovation. Be part of determining what’s right for your business. The very tools that your auditor employs to streamline procedures and continuously improve quality will generate a world of insights for your company that are not available without such technology.

If you would like to develop a deeper understanding, we’d be happy to provide a demonstration of how we are applying innovative technologies to audits today and help demonstrate how it’s about not just the quality of the audit — but also the quality of your experience with your auditor.

For more pragmatic insights, visit our Boards and audit committees page.

Share with your network

Share