On July 8, 2022, Pennsylvania Gov. Tom Wolf approved Act 53 (H.B. 1342), which primarily makes significant changes to the Pennsylvania Corporate Net Income Tax (CNIT). Specifically, the legislation gradually reduces the CNIT rate to 4.99% over a nine-year period, applies market-based sourcing rules for receipts from sales of intangible property, and establishes a statutory economic nexus standard with a $500,000 sales threshold for CNIT purposes.1 Additionally, the legislation conforms the personal income tax (PIT) to certain sections of the Internal Revenue Code (IRC), including the Sec. 179 expense deduction limitation and Sec. 1031 like-kind exchange treatment. Finally, the bill makes minor changes to the sales tax law and certain credit and incentive programs.

Corporate net income tax rate

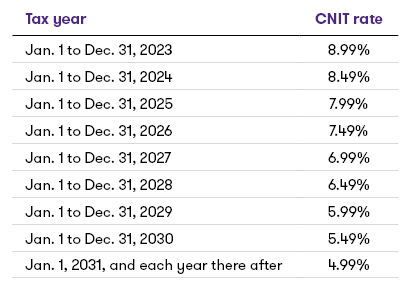

H.B. 1342 decreases the CNIT rate from the current 9.99% rate to 8.99% beginning with the 2023 tax year, and decreases the rate in 0.5% increments each subsequent year through the 2031 tax year, when a 4.99% rate is reached.2 The annual rate reductions apply as follows:

Market-based sourcing for intangible receipts

Prior to the enactment of Act 53, Pennsylvania law required that receipts from sales of intangible property be sourced primarily using a costs-of-performance method. Effective for tax years beginning after Dec. 31, 2022, the law adopts a market-based sourcing approach, bringing the sourcing rules in line with the current method used for sales of services.3 The legislation provides that gross receipts from the following types of transactions are sourced to Pennsylvania:

- Leases or licenses of intangible property to the extent used in Pennsylvania, including the sale or exchange of property where the receipts derive from payments contingent on the productivity, use, or disposition of the property4

- Sales of intangible property where the property sold is a contract right, government license or similar property authorizing the holder to conduct business activity in a specific geographic area, to the extent the property is used in or otherwise associated with the state5

- Sales, redemption, maturity, or exchanges of securities held by the taxpayer primarily for sale to customers in the ordinary course of its trade or business, if the customer is located in Pennsylvania6

- Interest, fees, and penalties imposed on loans secured by real property received by corporations that regularly lend funds to unaffiliated entities, to be calculated as follows:

- The sales factor numerator includes interest, fees and penalties, imposed in connection with loans secured by real property if the property is located within the state

- If the property is located in Pennsylvania and another state, gross receipts are included in the sales factor numerator if more than 50% of the fair market value of the real property is located in Pennsylvania

- Gross receipts are included in the sales factor numerator if more than 50% of the fair market value of the property is not located in any single state and the borrower is located in the state7

- Interest, fees and penalties from loans related to the sale of tangible personal property other than transportation property:

- The sales factor numerator includes receipts from interest, fees and penalties imposed if the property is delivered or shipped to a purchaser in Pennsylvania8

- Interest, fees and penalties from loans related to the sale of transportation property:

- An aircraft is deemed to be used in the state according to a ratio of in-state to total number of landings of the aircraft

- A motor vehicle is deemed to be used wholly in the state in which it is registered; and

- If the extent of use within Pennsylvania cannot be determined, the property is deemed to be used wholly in the state in which the property was delivered or shipped to the purchaser9

- Interest, fees and penalties from loans for sales not otherwise described if the borrower is located in Pennsylvania10

- Interest, fees and penalties from credit card receivables and credit card fees charged to cardholders if the cardholder’s billing address is in Pennsylvania11

- Interest not otherwise described in the law shall be included in the numerator of the sales factor if the lender’s commercial domicile is in Pennsylvania12

Gross receipts received from intangible property not otherwise described above are to be excluded from both the numerator and the denominator of the Pennsylvania sales factor.13 The Department is authorized to adopt regulations as necessary to implement the market-based sourcing rules.14

CNIT statutory economic nexus standard

Following the U.S. Supreme Court’s 2018 decision in South Dakota v. Wayfair,15 the Pennsylvania Department of Revenue (Department) issued Corporation Tax Bulletin 2019-04, which established an economic nexus standard for CNIT purposes effective beginning with the 2020 tax year.16 The policy created a rebuttable presumption of substantial nexus and a CNIT filing requirement for corporations having $500,000 or more in annual gross receipts sourced to Pennsylvania.17

Effective for tax years beginning on or after Jan. 1, 2023, the legislation codifies the Department’s economic nexus standard to establish a CNIT filing obligation.18 “Substantial nexus” is defined as any direct or indirect business activity sufficient to grant the Commonwealth authority under the U.S. Constitution to impose CNIT.19 Similar to the Department’s existing policy, the law establishes a rebuttable presumption of “substantial nexus” for a corporation with $500,000 or more of sales sourced to Pennsylvania without regard to physical presence in the Commonwealth.20 “Business activity” includes but is not limited to:

- Leasing or licensing intangible property utilized in the Commonwealth

- Regularly engaging in transactions with customers in the Commonwealth involving intangible property, including loans made by a corporation that regularly lends funds to unaffiliated entities or to individuals, or

- Sales of intangible property utilized by the corporation within the Commonwealth21

Foreign affiliated entities that have entered into a comprehensive U.S. income tax treaty providing for the allocation of all categories of income tax on royalties, licenses, fees and interest in order to prevent of double taxation are not subject to the substantial nexus standard.22

Personal income tax changes

The legislation conforms the Pennsylvania PIT to the following IRC provisions:23

- Conformity with the IRC Sec. 179 Expense Deduction: the expense deduction limit for property placed in service after Dec. 31, 2022, is increased from $25,000 to match the federal limit ($1,080,000 for 2022).24

- Conformity with IRC Sec. 1031 Like-Kind Exchange Treatment: gain from real property can be deferred in a qualifying like-kind exchange under Sec. 1031 for tax years beginning after Dec. 31, 2022.25 Previously, the recognized gain was taxable for PIT purposes.

Other notable provisions

Other notable provisions contained in Act 53 include the following:

- Effective Jan. 1, 2023, sales and use tax is imposed on peer-to-peer car sharing, whether through a shared vehicle owner, marketplace facilitator or rental company maintaining a place of business in Pennsylvania.26 However, peer-to-peer car sharing is excluded from the state’s 2% vehicle rental tax.27

- The qualification period for the Computer Data Center sales tax exemption is extended from 15 to 25 years for qualified purchases of equipment installed in a computer data center.28

- The legislation establishes and/or modifies various credit and incentive programs, including:

- Research and Development Tax Credit: annual cap increased from $55 million to $60 million (cap for allocations to small business increased from $11 million to $12 million);29

- Film Production Tax Credit: annual cap increased from $70 million to $100 million;30

- Entertainment Economic Enhancement Program: annual cap increased from $8 million to $24 million;31

- Waterfront Development Tax Credit: annual cap increased from $1.5 million to $5 million;32 and

- Airport Land Development Zone Program: established to promote economic growth and job creation at or around airports on undeveloped or vacant land and buildings owned by Pennsylvania airports. Employers located in designated Airport Land Development Zones are eligible for a tax credit equal to $2,100 for each full-time job created in the zone.33

- Keystone Opportunity Zone (KOZ) Program Changes: clarifies that an affiliate of a qualified business locating within a KOZ is entitled to the same tax exemptions, deductions, abatements, and credits provided to the qualified business.34 The law additionally provides for a one-year extension for a political subdivision to apply for a KOZ designation originally authorized by Act 13 of 2019.35

Commentary

The enactment of Act 53 represents the culmination of efforts by Governor Wolf and the Pennsylvania General Assembly to make substantial reductions to the CNIT rate, a longtime goal of the governor since the early days of his administration. The agreement on incremental CNIT rate reductions was possible in part due to a nearly $6 billion budget surplus for the 2022 fiscal year, in addition to $2.1 billion in federal COVID-19 relief funds allocated to the state by the American Rescue Plan Act.36 Although the Governor sought additional changes to the CNIT including amendments to the state’s related-party addback provisions as part of his proposed budget, those provisions ultimately did not make it into the enacted legislation. The projected revenue impact from the CNIT rate reductions is also partially offset by the sourcing changes to sales of intangible property and the codification of the Department’s economic nexus standard, resulting in an estimated $202 million revenue decrease for the 2023 fiscal year.37

The incremental CNIT rate reductions from the current 9.99% to 4.99% over a nine-year period is a significant development for Pennsylvania, a state with the second highest corporate income tax rate in the country behind only New Jersey. Unlike corporate income tax rate reductions enacted by other states over the past two years, the gradual CNIT rate reductions are not contingent on satisfying specific revenue targets in future tax years. While there was bipartisan support for the rate reductions, it will be interesting to see whether future governors and legislatures remain committed to the rate cuts as currently planned, or whether changing fiscal and economic conditions might change the timetable for these reductions.

Pennsylvania’s new detailed CNIT sourcing rules for sales of intangible property and certain financial transactions generally establish a market sourcing methodology in line with the existing rules in place for receipts from sales of services. Notably, the legislation contains an important “throwout” provision whereby gross receipts from intangible property not specifically described in the statute are excluded from the sales factor. Presumably, transactions including goodwill arising from the sale of a business and proceeds from hedging transactions are not addressed in the law and are potentially subject to throwout. Additionally, there are exceptions to the general market-based sourcing rules, including interest received by an affiliate from a Pennsylvania business where the affiliate is domiciled outside the state. While the Department is directed to promulgate regulations to implement the sourcing provisions, they are not expected anytime soon, given that the Department is in the process of finalizing regulations interpreting market-based sourcing rules for sales of services that have been in effect since 2014. The sourcing rules for sales of intangible property and services are not applicable to pass-through entities, which remain subject to cost-of-performance sourcing rules under the PIT law.

The legislation also codifies the Department’s CNIT economic nexus standard previously announced in Corporation Tax Bulletin 2019-04, containing a rebuttable presumption of substantial nexus for corporations having $500,000 in gross receipts sourced to Pennsylvania without regard to physical presence. Given that the statutory economic nexus standard is effective beginning with the 2023 tax year, the enforceability of the Department’s economic nexus policy during the 2020-2022 tax years remains an open question and potentially subject to taxpayer challenge. Should the policy be challenged, one of the primary questions will be the extent of the Department’s authority under Wayfair to adopt an economic nexus standard for CNIT purposes. As with the newly established sourcing rules for sales of intangible property, the economic nexus standard does not apply for PIT purposes.

Notably absent from the budget legislation was a provision that would have established an elective pass-through entity tax regime, making Pennsylvania the largest state without such an entity-level tax to date. The budget package also lacked the required authorizing legislation that would allow the City of Philadelphia to extend the net operating loss carryforward period from the current three years to 20 years for purposes of the city’s Business Income and Receipts Tax. However, both measures may be taken up again when the General Assembly reconvenes this coming fall.

As a result of the CNIT rate reductions and changes to sourcing rules for sales of intangibles, there are important financial statement impacts for corporate taxpayers to consider beginning with the third quarter of 2022, in addition to tax accounting and planning opportunities to defer income to future years featuring lower rates, and likewise accelerating deduction to earlier tax years when higher rates are in effect. For apportionment purposes, corporate taxpayers generating intangible income may consider how the new intangible sourcing rules may impact their Pennsylvania sales factor, especially in years when large gains are expected. For example, out-of-state taxpayers that historically sourced intangible income outside of Pennsylvania may see an increased sales factor to the extent that the intangible property is used in or associated with the state. Conversely, in-state taxpayers engaging in transactions involving intangible property used outside the state may have opportunities to reduce their sales factor, resulting in potential changes to CNIT liability and associated financial statement impact.

1 Pa. Act 53 (H.B. 1342), Laws 2022.

2 H.B. 1342, § 7, amending 72 PA. STAT. § 7402(b).

3 H.B. 1342, § 6, amending 72 PA. STAT. § 7401(3)2.(a)(17). The interpretation of the cost-of-performance sourcing rules for sales of services prior to the 2014 tax year is currently the subject of dispute in Synthes USA HQ, Inc. v. Commonwealth, a case pending before the Pennsylvania Supreme Court. Most recently, the Pennsylvania Commonwealth Court endorsed the Department’s policy equating cost-of-performance sourcing to market-based sourcing for sourcing service receipts, rejecting arguments by the Pennsylvania Attorney General’s office to the contrary. 236 A.3d 1190 (Pa. Commw. Ct. 2020). For further discussion of the Synthes case, see GT SALT Alert: Pennsylvania court upholds Revenue Dept. sourcing method.

4 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(C). The term “intangible property” is not specifically defined.

5 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(D).

6 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(E).

7 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(F).

8 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(G).

9 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(G)(ii).

10 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(H).

11 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(I).

12 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(J).

13 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(K).

14 H.B. 1342, § 6, adding 72 PA. STAT. § 7401(3)2.(a)(17)(L).

15 138 S. Ct. 2080 (2018).

16 Corporation Tax Bulletin 2019-04, Nexus for Corporate Net Income Tax Purposes, Pa. Department of Revenue, Sept. 30, 2019, rev. Aug. 6, 2020.

17 Id.

18 H.B. 1342, § 7, adding 72 PA. STAT. § 7402(a)(5).

19 H.B. 1342, § 7, adding 72 PA. STAT. § 7402(a)(5)(I).

20 H.B. 1342, § 7, adding 72 PA. STAT. § 7402(a)(5)(III).

21 H.B. 1342, § 7, adding 72 PA. STAT. § 7402(a)(5)(II).

22 H.B. 1342, § 7, adding 72 PA. STAT. § 7402(a)(6).

23 Given that Pennsylvania taxable income is not derived from federal taxable income for PIT purposes, IRC provisions must be specifically adopted in the PIT law.

24 H.B. 1342, § 4, amending 72 PA. STAT. § 7303(a.3).

25 H.B. 1342, § 4, amending 72 PA. STAT. § 7303(a.5).

26 H.B. 1342, § 1, amending 72 PA. STAT. § 7201(b), (k), (n), (o), (p).

27 H.B. 1342, § 7, amending 72 PA. STAT. § 8602-A.

28 H.B. 1342, § 18, amending 72 PA STAT. § 9931-D(D).

29 H.B. 1342, § 7, amending 72 PA. STAT. § 8709-B.

30 H.B. 1342, § 10, amending 72 PA. STAT. § 8716-D(a).

31 H.B. 1342, § 11, amending 72 PA. STAT. § 8777-D.

32 H.B. 1342, § 12, amending 72 PA. STAT. § 8708-K.

33 H.B. 1342, § 15, adding 72 PA. STAT. § 8901-H.

34 H.B. 1342, § 13, amending 72 PA. STAT. § 8912-D.

35 H.B. 1342, § 14, amending 72 PA. STAT. § 8921-D.

36 Press Release: Record Revenues Will Cover Historic Education Investment with Billions Left Over, Office of Gov. Tom Wolf, June 1, 2022.

37 H.B. 1342 Fiscal Note, Pa. House Appropriations Committee, July 7, 2022.

Contacts:

Tax professional standards statement

This content supports Grant Thornton LLP’s marketing of professional services and is not written tax advice directed at the particular facts and circumstances of any person. If you are interested in the topics presented herein, we encourage you to contact us or an independent tax professional to discuss their potential application to your particular situation.

Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein. To the extent this content may be considered to contain written tax advice, any written advice contained in, forwarded with or attached to this content is not intended by Grant Thornton LLP to be used, and cannot be used, by any person for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

The information contained herein is general in nature and is based on authorities that are subject to change. It is not, and should not be construed as, accounting, legal or tax advice provided by Grant Thornton LLP to the reader. This material may not be applicable to, or suitable for, the reader’s specific circumstances or needs and may require consideration of tax and nontax factors not described herein. Contact Grant Thornton LLP or other tax professionals prior to taking any action based upon this information.

Changes in tax laws or other factors could affect, on a prospective or retroactive basis, the information contained herein; Grant Thornton LLP assumes no obligation to inform the reader of any such changes. All references to “§,” “Sec.,” or “§” refer to the Internal Revenue Code of 1986, as amended.

Trending topics

Share with your network

Share