The FASB recently issued ASU 2023-02, Accounting for Investments in Tax Credit Structures Using the Proportional Amortization Method (a consensus of the Emerging Issues Task Force), which allows an entity to elect to use the proportional amortization method to account for qualifying equity investments in tax credit structures that meet specified criteria, without regard to the underlying tax credit program. Previously, this method of accounting was only available for qualifying equity investments in low income housing tax credit (LIHTC) structures.

In addition to expanding the scope of the proportional amortization method, the amendments also impact the accounting for existing equity investments in LIHTC structures that were not previously accounted for using the proportional amortization method.

Proportional amortization method

Under the proportional amortization method, the initial cost basis of a qualifying equity investment must be amortized in proportion to the income tax credits and other income tax benefits received. In addition, the amortization of the investment’s cost basis and the income tax credits is presented net in the income statement as a component of income tax expense (benefit).

Use of proportional amortization method expanded

The amendments in ASU 2023-02 comprise a consensus reached by the FASB’s Emerging Issues Task Force (EITF), which was subsequently ratified by the FASB, to amend existing guidance so that equity investors in a tax credit structure, regardless of the related tax credit program, may now elect to use the proportional amortization method to account for their tax equity investments if certain conditions are met.

The election is made on a program-by-program basis.

Conditions to apply proportional method

An equity investor in a tax equity structure may only apply the proportional amortization method if all of the following conditions in ASC 323-740-25-1 are met:

- It is probable that the income tax credits that will be allocated to the investor will be available.

- The investor does not have the ability to exercise significant influence over the operating and financial policies of the underlying project.

- Substantially all of the projected benefits are from income tax credits and other income tax benefits. Refundable tax credits must be included in total projected benefits but must be excluded from income tax credits and other income tax benefits.

- The investor’s projected yield, based solely on the cash flows from the income tax credits and other income tax benefits, is positive.

- The investor is a limited liability investor for both legal and tax purposes, and the investor’s liability is limited to its capital investment.

Delayed equity contributions

The amendments also require entities using the proportional amortization method for qualifying investments to apply the delayed equity contribution guidance in ASC 323-740-25-3, which requires that a liability be recognized for delayed equity contributions that are either (1) unconditional and legally binding, or (2) contingent upon a future event once that contingent event becomes probable.

If the proportional amortization method is not applied, entities are no longer permitted to use the guidance on delayed equity contributions, which impacts investors in LIHTC structures who may have applied the delayed equity contributions guidance without electing the proportional amortization method before adopting the new amendments.

Disclosures

The amendments further require an entity to disclose information about all investments that generate income tax credits and other income tax benefits from a tax credit program accounted for using the proportional amortization method in accordance with ASC 323-740, including investments within that elected program that do not meet the conditions to apply the proportional amortization method.

The amendments require that an entity disclose information in annual and interim reporting periods, including

- The nature of its tax equity investments

- The effect of its tax equity investments and related income tax credits and other income tax benefits on its financial position and results of operations

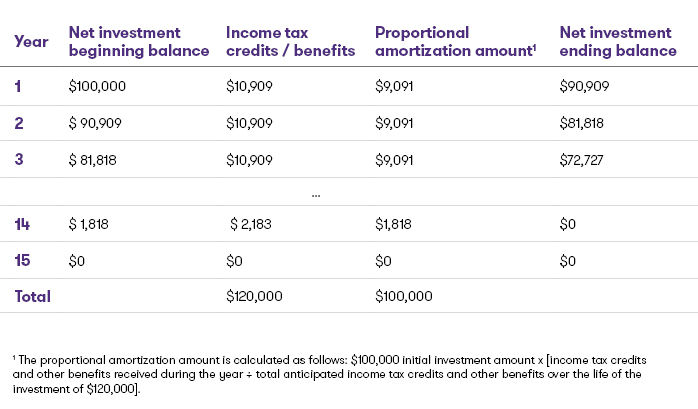

Illustration

The following scenario is an abbreviated version of the example in ASC 323-740-55-2 through 55-5 that illustrates how to apply the proportional amortization method. Assume the following facts:

- The purchase price of 5 percent equity investment in a limited partnership interest in the project is $100,000.

- The total projected income tax credits and other income tax benefits to be received over the 15-year period equal $120,000.

Based on this scenario, the below table shows income tax credits and other income tax benefits received within each year.

For the years shown, the net amount presented in the income tax expense (benefit) line item would equal

- $1,818 for each of the first three years, equal to $10,909 in income tax credits and other benefits minus $9,091 of amortization during each year

- $365 in Year 14, equal to $2,183 in income tax credits and other benefits minus $1,818 of amortization

- $0 in Year 15, equal to $0 in income tax credits and other benefits minus $0 of amortization

Application of other GAAP

As a result of the amendments, the guidance in ASC 323-740 applies only to tax equity investments accounted for using the proportional amortization method. Equity investors in qualifying LIHTC structures who previously could apply ASC 323-740, even if the proportional amortization method was not applied, are no longer able to do so upon adoption of the new amendments.

Therefore, absent an election to apply the fair value option, investors in equity investments in tax equity structures to which the proportional amortization method is not applied now need to determine whether the guidance in either ASC 323, Investments – Equity Method and Joint Ventures, or in ASC 321, Investments – Equity Securities, is applicable and apply that guidance in its entirety, including the impairment guidance. Under either Topic, investment income, gains and losses, and tax credits must be presented gross on the income statement, rather than netted in the income tax expense (benefit) line item.

Effective date and transition

For public business entities, the amendments are effective for fiscal years beginning after Dec. 15, 2023, including interim periods within those fiscal years. For all other entities, the amendments are effective in fiscal years beginning after Dec. 15, 2024, including interim periods within those fiscal years. All entities are permitted to early adopt the amendments in any interim period as of the beginning of the fiscal year.

Entities must transition to the new guidance on either a modified retrospective or a retrospective basis. An investor who has not previously applied the proportional amortization method to LIHTC investments (and, therefore, can no longer apply the guidance in ASC 323-740 after adopting the amendments) may elect a prospective approach rather than its general transition method.

Contacts:

Partner & Chief Accountant, Grant Thornton LLP

Partner, Grant Thornton Advisors LLC

Graham Dyer serves as Grant Thornton LLP’s Chief Accountant. In this role, he leads the firm’s national Accounting Principles Group, which is responsible for Grant Thornton’s interpretation of accounting matters in both US Generally Accepted Accounting Principles (US GAAP) and International Financial Reporting Standards (IFRS).

Dallas, Texas

Industries

- Asset Management

- Banking

- Not-for-profit & Higher Education

- Private Equity

- Construction & Real Estate

Service Experience

- Audit & Assurance Services

Partner, Grant Thornton LLP

Partner, Grant Thornton Advisors LLC

Rahul is a Partner in the National Professional Standards Group (NPSG) of Grant Thornton. Rahul assists engagement teams and clients with technical accounting issues and monitors current accounting developments, under both U.S. GAAP and IFRS.

Chicago, Illinois

Industries

- Construction & Real Estate

- Manufacturing

- Technology

- Energy

- Retail & Consumer Brands

Service Experience

- Audit & Assurance Services

© 2023 Grant Thornton LLP, U.S. member firm of Grant Thornton International Ltd. All rights reserved.

This Grant Thornton LLP bulletin provides information and comments on current accounting issues and developments. It is not a comprehensive analysis of the subject matter covered and is not intended to provide accounting or other advice or guidance with respect to the matters addressed in the bulletin. All relevant facts and circumstances, including the pertinent authoritative literature, need to be considered to arrive at conclusions that comply with matters addressed in this bulletin. For additional information on topics covered in this bulletin, contact your Grant Thornton LLP professional. Portions of FASB Accounting Standards Codification® material included in this work are copyrighted by the Financial Accounting Foundation, 801 Main Avenue, P.O. Box 5116, Norwalk, CT 06856-5116, and are reproduced with permission.

Trending topics

Share with your network

Share