The SEC issued a Final Rule, Facilitating Capital Formation and Expanding Investment Opportunities by Improving Access to Capital in Private Markets, to simplify, harmonize, and improve the exempt offering framework under the Securities Act of 1933. The amendments are intended to reduce complexities, promote capital formation, and expand investment opportunities while maintaining investor protections.

The amendments are effective 60 days after publication in the Federal Register.

Grant Thornton insight

The existing exempt offering framework was created over 50 years through a patchwork of Congressional acts and SEC rules. While the Final Rule intends to make the framework more consistent, we encourage companies planning exempt offerings to consult with qualified securities counsel.

Integration framework

The Final Rule amends Rule 152, Integration, to simplify the integration framework used to determine whether multiple securities offerings that occur either concurrently or close in time (whether registered or exempt) should be considered part of the same offering. The amendments eliminate the five-factor test and replace it with a new general principle that looks to the particular facts and circumstances of each offering to make this determination.

Offering communications

The Final Rule amends the offering communications rules by expanding the use of the “test-the-waters” accommodation for offerings under Regulation Crowdfunding. The amendments permit an issuer to use non-specific solicitation-of-interest materials to “test-the-waters” before selecting an exemption method, and provide that certain “demo day” communications are not deemed to be general solicitation or general advertising.

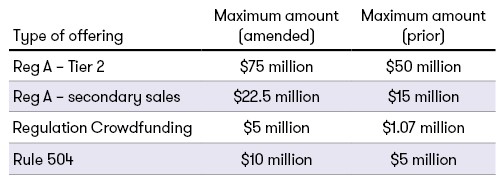

Offering and investment limits

The Final Rule amends certain maximum offering amounts as shown in the following table.

The amendments also restrict registrants that are delinquent in their reporting obligations under the Securities Exchange Act of 1934 from conducting exempt offerings under Regulation A.

Further, the Final Rule extends the period of relief for an additional 18 months provided under the Temporary Amendments to Regulation Crowdfunding (PDF - 1.88KB), which exempts certain financial statement review requirements for Regulation Crowdfunding offerings of $250,000 or less within a 12-month period. The extension is effective upon the Final Rule’s publication in the Federal Register.

Download (PDF - 234.12KB) a printable version of this article here.

Contacts:

National Managing Partner of Professional Practice, Audit Services

Partner, Audit Services, Grant Thornton LLP

Partner, Grant Thornton Advisors LLC

Kendra Decker is the national managing partner of Grant Thornton LLP’s Professional Practice within the firm’s Audit Quality and Risk group.

Partner-in-charge, SEC Regulatory Matters

Partner, Audit Services, Grant Thornton LLP

Partner, Grant Thornton Advisors LLC

Rohit Elhance is a partner in SEC Regulatory Matters group, with more than 17 years of international experience serving large multinational and entrepreneurial companies in the areas of audit, risk advisory and transaction services.

Washington DC, Washington DC

Industries

- Construction & Real Estate

- Manufacturing

- Technology

- Energy

Service Experience

- Advisory Services

- Audit & Assurance Services

- Transaction Advisory

© 2020 Grant Thornton LLP, U.S. member firm of Grant Thornton International Ltd. All rights reserved.

This Grant Thornton LLP bulletin provides information and comments on current accounting issues and developments. It is not a comprehensive analysis of the subject matter covered and is not intended to provide accounting or other advice or guidance with respect to the matters addressed in the bulletin. All relevant facts and circumstances, including the pertinent authoritative literature, need to be considered to arrive at conclusions that comply with matters addressed in this bulletin. For additional information on topics covered in this bulletin, contact your Grant Thornton LLP professional.

Share with your network

Share