The FASB recently issued ASU 2021-04 to codify the final consensus reached by the Emerging Issues Task Force (EITF) on how an issuer should account for modifications made to equity-classified written call options (hereafter referred to as a warrant to purchase the issuer’s common stock). The guidance in the ASU requires the issuer to treat a modification of an equity-classified warrant that does not cause the warrant to become liability-classified as an exchange of the original warrant for a new warrant. This guidance applies whether the modification is structured as an amendment to the terms and conditions of the warrant or as termination of the original warrant and issuance of a new warrant.

Measurement

Under the amendments, an issuer should measure the effect of a modification as the difference between the fair value of the modified warrant and the fair value of that warrant immediately before modification.

Recognition

The EITF concluded that the recognition of the modification depends on the nature of the transaction in which a warrant is modified. If there is more than one element in a transaction (for example, if the modification involves both a debt modification and an equity issuance), then the guidance requires the issuer to allocate the effect of the option modification to each element.

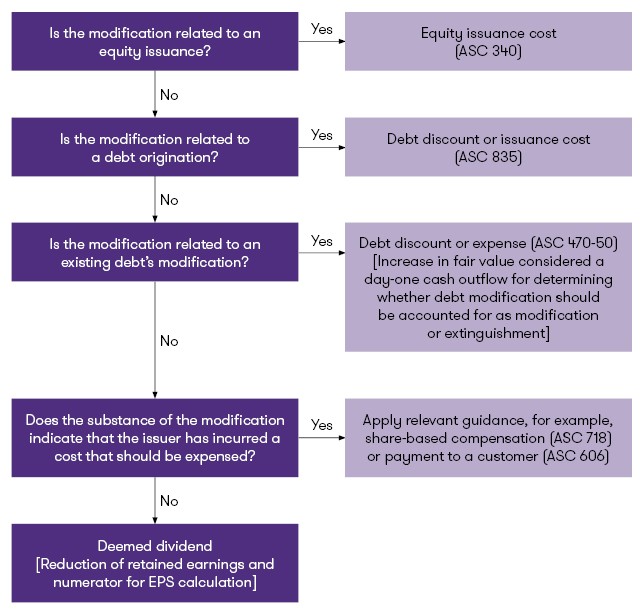

Equity issuance

If a warrant is modified in connection with an equity issuance, the issuer should recognize the increase (and disregard any decrease) in the warrant’s fair value as deferred costs of an equity offering (that is, as an equity issuance cost in accordance with ASC 340, Other Assets and Deferred Cost), which should be charged against the gross proceeds of the offering.

Debt origination

If a warrant is modified in connection with the origination of debt, the issuer should recognize the increase (and disregard any decrease) in the warrant’s fair value as a debt discount if the warrants are held by the lender, or as debt issuance cost if the warrants are held by a third-party, and should account for them in accordance with ASC 835 in determining the effective interest rate on the new debt.

Debt modification

If the warrant’s modification is part of, or directly related to, an existing debt’s modification within the scope of ASC 470-50 and ASC 470-60, then the recognition is based on whether the warrant is held by a creditor or by a third party, as follows:

- If the warrant is held by a creditor involved in the debt modification, the issuer should treat the warrant’s change in fair value as a fee paid to, or received from, the creditor. The issuer should include the difference (that is, any increase or decrease) in the warrant’s fair value in calculating the effective borrowing rate of the new debt when assessing whether a concession is granted under ASC 470-60 and, if the debt modification is within the scope of ASC 470-50, in applying the 10 percent test to determine whether the debt modification is substantial.

- If the warrant is held by a third party, then the issuer should treat an increase in the warrant’s fair value as a third-party cost and should disregard any decrease.

Modification unrelated to equity issuance and debt origination or modification

For other types of warrant modifications, the issuer should recognize the increase (and disregard any decrease) in the warrant’s fair value as a deemed dividend, unless the modification is within the scope of other Codification topics. For example, compensation for goods and services should be accounted for under ASC 718, and a transaction with a customer should be accounted for under ASC 606.

If a modification or an exchange of a warrant is not related to a financing or compensation for goods or services, then the modification should be accounted for in accordance with its substance. For example, in paragraph 19 of the Basis for Conclusions to ASU 2021-04, the EITF also concluded that if an issuer modifies a warrant in exchange for an agreement by the holder to abandon certain acquisition plans, to forgo other planned activities, to settle litigation or employment contracts, or to voluntarily restrict the warrant holder’s purchase of the issuer’s (or its affiliate’s) shares, then those rights and privileges obtained, both stated and unstated, as well as other elements under such transaction, should be accounted for based on their substance. Note that this accounting might result in the issuer recognizing an expense rather than a dividend distribution.

An issuer that presents earnings per share (EPS) should deduct the effect of a warrant modification recognized as a deemed dividend in computing income or loss available to common stockholders as part of the basic EPS calculation.

Effective date

The guidance is effective for fiscal years beginning after Dec. 15, 2021, including interim periods within those fiscal years. Early application is permitted, including in an interim period as of the beginning of the fiscal year that includes that interim period.

Transition and transition disclosures

Entities should apply the guidance prospectively to modifications that occur after the date of initial application.

Entities should provide transition disclosures consistent with the guidance in ASC 250, Accounting Changes and Error Corrections, except for the effect of adoption on the financial statement line items, including EPS for the current period and for any prior periods retrospectively adjusted.

Contacts:

Rahul Gupta

Partner, National Professional Standards Group

Rahul is a Partner in the National Professional Standards Group (NPSG) of Grant Thornton LLP. Rahul assists engagement teams and clients with technical accounting issues and monitors current accounting developments, under both U.S. GAAP and IFRS.

Chicago, Illinois

Industries

- Construction & real estate

- Manufacturing, Transportation & Distribution

- Technology, media & telecommunications

- Energy

- Retail & consumer brands

Service Experience

- Audit & Assurance

© 2021 Grant Thornton LLP, U.S. member firm of Grant Thornton International Ltd. All rights reserved.

This Grant Thornton LLP bulletin provides information and comments on current accounting issues and developments. It is not a comprehensive analysis of the subject matter covered and is not intended to provide accounting or other advice or guidance with respect to the matters addressed in the bulletin. All relevant facts and circumstances, including the pertinent authoritative literature, need to be considered to arrive at conclusions that comply with matters addressed in this bulletin. For additional information on topics covered in this bulletin, contact your Grant Thornton LLP professional.

Our audit insights

No Results Found. Please search again using different keywords and/or filters.