By fits and starts, the global economy is starting to stabilize, bringing along a retail and consumer industry that has been hit as hard as any. With growth and recovery come opportunities, often in the form of mergers and acquisitions.

According to PitchBook Data, Inc.* data, deal volume for the retail sector increased in 2021 from 2020 levels of activity: In 2021, 510 deals were completed, up from 369 deals in 2020. To gauge just how strong future M&A trends are expected to be in retail, Grant Thornton surveyed M&A professionals who regularly work on retail and consumer deals for their perspectives on retail M&A activity in 2022. In general, respondents see the first half of 2022 as an active one for retail and consumer deals, with both increasing activity and increasing valuation of those deals.

Within that general positive activity lie some caveats. Our survey respondents emphasized these points about the retail and consumer M&A environment:

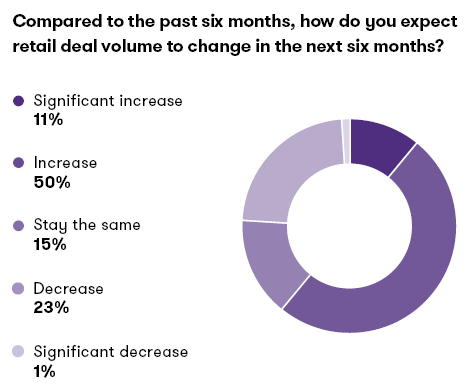

- Nearly two-thirds expect an increase in deal volume in the next six months.

- Half thought valuations also will increase, with only 14% expecting a decrease in valuations.

- Supply chain constraints, however, pose challenges, as more than half of respondents say supply chain issues have delayed or terminated transactions.

- Businesses with both brick-and-mortar and e-commerce operations are seen as the most likely to be involved in deals.

- The Biden administration financial, investment and trade policies are seen to be the most favorable to retail deal activity, with labor, general taxation and corporate rate policies seen as the most unfavorable to retail deal activity.

- Respondents are divided on the impact of international tax policies on deal activity.

- Respondents think capital gains increases will spur M&A activity, but a phaseout of the pass-through deduction would have a dampening effect.

M&A funds are already in place

Simon Jewkes, Strategy and Transactions Principal at Grant Thornton, said the expected volume of near-future retail M&A activity is likely being driven by an unprecedented level of cash flowing into private equity funds over the last three years. That availability of dry powder creates its own pressure to use it. A separate general Grant Thornton survey of M&A professionals indicates private equity respondents expect this trend to continue.

“The economy is doing well and the banks are lending, so the environment to do deals is good,” Jewkes said. “Perhaps people were thinking that the COVID-19 situation was going to be better,” Jewkes, said, adding that the Omicron variant wave and its consequent jolt to the American economy, including the stock market, happened right after our survey was fielded. But with more people vaccinated, Jewkes said there is a different mindset among many leaders who nonetheless are ready to make deals that leverage the vast amount of money already raised.

Kevin Kelly, Retail National Managing Partner at Grant Thornton, said a belief that M&A activity will increase also is suggested by the massive growth in the creation of SPAC investments. Kelly said SPACs became hugely popular in the pandemic given the challenges to do more traditional transactions. As a result, it is time to make a deal or potentially refund monies raised through SPACs in the past year or so.

Even though the SPAC market has slowed recently, a trend that is expected to continue, the proliferation of SPACs in the past two years, combined with the flush of private equity funds poised to make a move, adds to why industry leaders and investors think the retail industry could be in line for continued strong M&A activity in 2022.

M&A funds are already in place

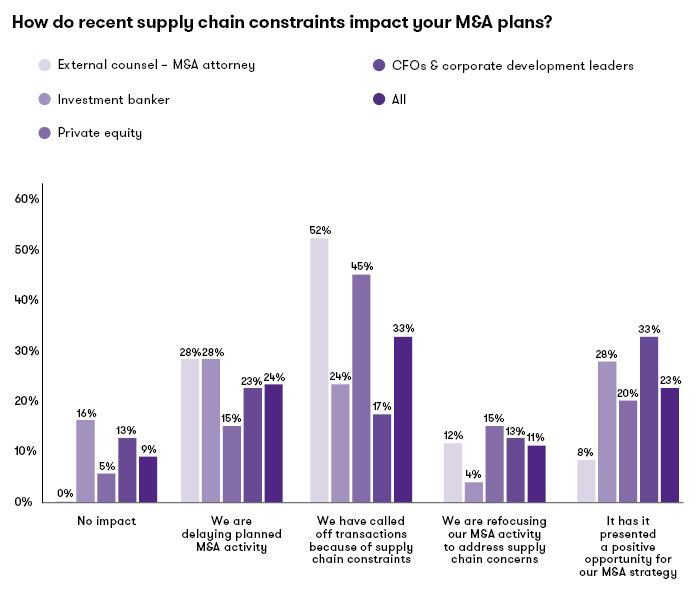

One notable exception to this overarching deal-related optimism is the ongoing pandemic-related supply chain disruptions. Our survey noted that more than half (57%) of respondents indicated they were either delaying or had called off deals due to supply chain constraints.

Also instructive is the breakdown of those answering. M&A attorneys and private equity leaders, who likely saw more overall transactions, answered the supply chain impact question much more negatively than investment bankers and C-suite leaders. Corporate executives in particular think supply chain disruption more likely presented positive opportunities for deals. Jewkes said that may indicate that C-suite leaders in companies with a secure supply chain might benefit from acquiring another company that has supply chain disruptions if the buyer has the capacity to solve those issues. Reversing that, Kelly said an acquiring company could be attracted to a target that could help solve a particular supply chain issue. In those ways, supply chain issues in a company could be a merger/acquisition incentive.

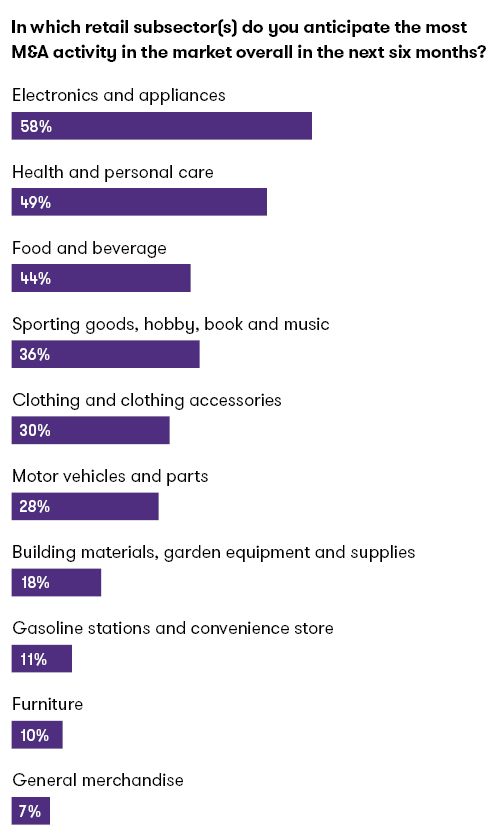

When our survey asked which retail subsectors are anticipated to have the most M&A activity, those included: 1) electronics and appliances, 2) health and personal care, 3) food and beverage and 4) sporting goods, hobbies, books and music.

Jewkes said the interest in these subsectors is not surprising since pent-up consumer demand, fueled by increased personal savings rates, will continue to be unleashed on non-essential items like technology and leisure items, so activity in those industries would logically follow. “If there’s anything with technology, either smart home devices or other types of electronics and technology devices, I think organizations are interested in that space and investing there.”

Elliot Findlay, National Managing Principal of Mergers & Acquisitions for Grant Thornton, ties strong M&A activity in these sectors to a trend in consumers’ increased willingness to return to in-person experiences, including retailers that feature in-store attractions. Retailers that entice consumers to step foot in their stores by providing an entertainment experience such as live music, captivating video displays and upscale dining – “experiential retail” – are companies he is seeing regularly in recent M&A transactions.

Meanwhile, the retail subsectors of furniture, general merchandise, gas stations and convenience stores are not expected to experience as much M&A activity.

When asked whether brick-and-mortar or e-commerce retail businesses would see the majority of M&A activity, 60% of respondents say businesses with a combination of both would likely see the most activity. This echoes past experience of retail leaders that they need to meet customers where they are and provide them multiple ways to buy goods, given their increased expectations around purchasing flexibility. This data underscores the importance of the brick-and-mortar store and its position as a complement to the brand’s e-commerce platform.

Taxation complications

Though the federal reconciliation bill, and its significant tax implications, are currently on life support, there is no question tax law changes will remain a central policy concern of the Biden administration. When asked how various tax policy questions would affect retail M&A activity, one answer that stood out was that respondents see a capital gains rate increase likely to be a net positive for M&A transactions, even though it would seem to take money out of the deals.

“The answer is not that a capital gains tax increase is good for retail, but it may spur current M&A activity to recognize capital gains before an increase,” said Candice Turner, National Managing Principal of M&A Tax Services at Grant Thornton. “A constant credible threat of increased rates would encourage M&A activity.” This way, a capital gains rate increase would spur M&A activity in the short term as a way of managing assets and see an increase in tax-deferred mergers and acquisitions over the long term.

Survey respondents see a phase-out of the pass-through deduction and an increase of the individual income tax rate as having a mostly negative impact on M&A activity. These taxes are now less likely to happen in 2022, so reservations about any negative effects would be lessened, Turner said.

Opinions are evenly divided on two tax issues with international implications, the 15% global minimum tax and overall international tax regulations. Unlike domestic tax rate hikes, international taxes have been the recent focus of significant change. The U.S. and most other nations backed the OECD pillars creating a 15% minimum tax and an online sales tax framework. In December 2021, the IRS completed an overhaul of the rules governing various international tax law changes instituted by the Tax Cuts and Jobs Act.

Turner added that companies contemplating mergers should realize that often the majority of taxation concerns won’t be federal but involve state and local taxes. “More than half the time, the problems we see in deals involve the target organization’s state and local tax position, including failure to file in states where the target has economic nexus and outstanding liabilities. The complications of state and local tax have made complete compliance almost impossible,” Turner said. “That’s really impacting M&A activity right now.” What’s unmistakable in this survey data is that industry professionals see retail companies as full participants in M&A deals in 2022. Company leaders examining the retail and consumer business environment should closely evaluate the risks and benefits of a deal, and in doing so, consider outside help to discern the best path forward.

*Source: PitchBook Data Inc.

Contacts:

Our featured insights

No Results Found. Please search again using different keywords and/or filters.