What we have learned over the years valuing earnouts

A robust M&A market, impacted by COVID-19 concerns, has highlighted the importance of the valuation of earnouts. A recent Grant Thornton survey report confirmed this, identifying earnouts as the source of over one-half of all M&A disputes. But proper valuations of earnouts still remain a challenge. Many acquirers and sellers overestimate the earnout value during the transaction negotiations and determination of deal value. In addition, unclear earnout definitions and terms often result in future legal disputes.

“It’s important to get the earnout accounting and valuation right, upfront, and cut down on the disputes,” said Elliot Findlay, Mergers & Acquisitions national managing principal at Grant Thornton. Fortunately, many current disputes can be avoided or minimized by shifting from scenario-based forecasting to option-pricing models such as Monte Carlo simulations.

The limitations of scenario-based approaches

Many current disputes can be avoided or minimized by shifting from scenario-based forecasting to option-pricing models such as Monte Carlo simulations.

More often than not, the acquirers use a simplified approach to approximate the value of the earnout when setting the earnout terms and deal price. Similarly, based on the existing forecast, the sellers believe that they are receiving a much higher value for their business (including the earnout). Such an approach fails to account for the risk inherent in the payout structure and the ability to achieve the forecast. It also often leaves out the counterparty risk, which is a risk additional to the discount rate that accounts for the time value of money.

The scenario-based method is typically ill-suited to earnout valuation because it considers too few outcomes. A limited number of scenarios is usually insufficient to capture the specific structure of the earnout, which often resembles an option (i.e., promising a payoff when a certain threshold is achieved). Furthermore, factors such as the historical volatility of and the risk associated the underlying metric(s) are either ignored or reflect management optimism, significantly overvaluing the earnout and goodwill at the time of the transaction.

Further issues occur when the scenario-based method is applied to value an earnout with asymmetrical payouts, which incorporate thresholds or hurdles, caps, catch-ups and other similar features. When earnouts are capped, a shortfall reduces the payment, but exceeding the cap adds nothing to the payment. When earnouts must clear a threshold or hurdle, small overperformance adds only marginal value, while a small shortfall can eliminate the earnout payout altogether. In such instances, the selected methodology makes a significant difference in the value of the earnout, and small decisions about classification and definition, as well as operational choices, can have significant consequences — and provoke conflict.

Sellers have a significant incentive to increase performance in the chosen metrics; buyers have an incentive to decrease it through strategy, accounting decisions. And, in rare cases, either party can influence the outcome through fraud.

The strengths of option-pricing models

By considering a potential range of outcomes rather than an optimistic forecast or a handful of discrete scenarios, a Monte Carlo simulation delivers more consistently accurate valuations.

By considering a potential range of outcomes rather than an optimistic forecast or a handful of discrete scenarios, a Monte Carlo simulation delivers more consistently accurate valuations. Such valuations better account for the historical and expected future volatility of revenue and earnings. This is why the authoritative Valuations in Financial Reporting Valuation Advisory 4: Valuation of Contingent Consideration published by The Appraisal Foundation recommends the option-pricing methodologies, including a Monte Carlo simulation, in the valuation of revenue and earnings earnouts.

The example illustrates the strengths of the Monte Carlo approach.

Earnout example

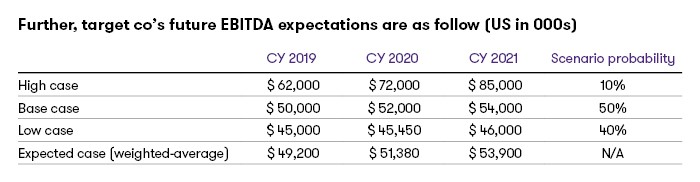

On Dec. 31, 2018, AcquirerCo closed a deal to acquire TargetCo. The terms of the deal include an earnout with the following terms:

- Earnout is based on annual earnings before interest, taxes, depreciation and amortization (EBITDA) targets for FY19, FY20 and FY21.

- A $5 million payment is made in any year TargetCo meets or exceeds forecasted EBITDA.

- Earnout payment, if earned, is made 120 days following the end of each period.

- Funds for potential earnout payment are not held in escrow and are subject to the acquirer’s credit risk.

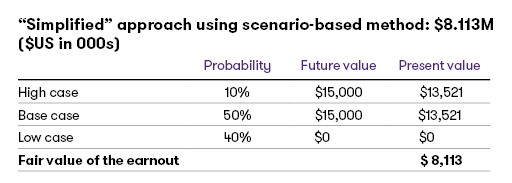

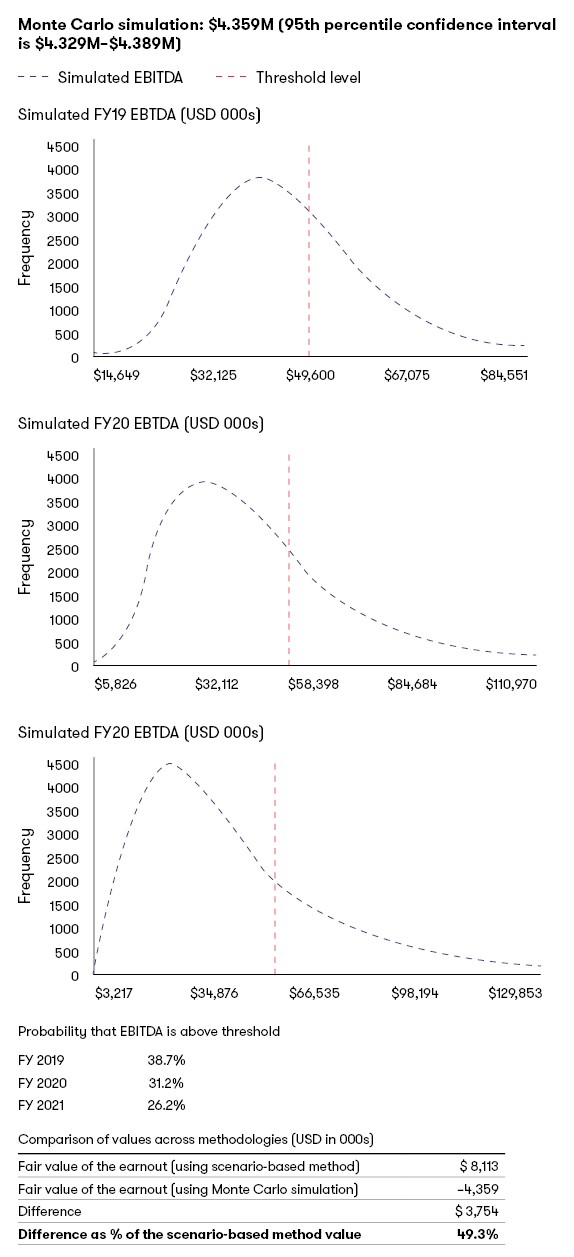

Following are the fair values of the earnout from the application of two different approaches — a scenario-based method and a Monte Carlo simulation.

Note the assumptions: 10.0% EBITDA discount rate, 4.5% risk-adjusted discount rate, 40.0% EBITDA volatility (only applicable to Monte Carlo simulation).

The importance of metrics and industry

In addition to the drawbacks noted, the scenario-based method does not sufficiently account for the effect of the risk and volatility of the underlying metrics of the earnout, including the industry-specific characteristics of the acquired company.

Since share price volatility is usually easily observed based on historical traded prices of comparable industry companies, price volatility typically serves as the starting point of volatility estimates for other metrics, such as EBITDA and revenue.

Simply put, volatility and risk increase as you go down the income statement. Revenues pose relatively low volatility and modest risks while EBITDA, which introduces operational leverage, poses higher volatility and more risk. By adding financial leverage in moving down the income statement from EBITDA to net income and price per share, net income and price introduce an even higher level of volatility and risk.

Since share price volatility is usually easily observed based on historical traded prices of comparable industry companies, price volatility typically serves as the starting point of volatility estimates for other metrics, such as EBITDA and revenue. To determine EBITDA volatility, share price volatility is adjusted for financial leverage. Similarly, to determined revenue volatility, share price volatility is adjusted for both financial leverage and operational leverage.

Since operational leverage differs from one industry to another, the same price volatility for two companies with vastly different operational leverage will result in significantly different revenue volatility. One company with large operational leverage (high fixed costs) may have a less risky revenue-based earnout; another company with very low operational leverage may have a very risky revenue-based earnout, all else equal.

While both parties have differing interests in earnouts — one company’s risk is another’s leverage — they have a shared interest in avoiding unnecessary disputes, which can be costly and distracting. Acquiring companies have an obvious interest in setting caps that limit the earnout payout. Target companies have an interest in renegotiating caps that deprive them of the benefit of predictably robust performance and hurdles that eliminate payouts for de minimis shortfalls in revenues and earnings. Overestimating the earnout as of the transaction date will overestimate the goodwill, making the early impairment more probable. As such, it is important to consider the facts outlined above when negotiating and valuing the earnout as of the transaction date.

Oksana Westerbeke, Valuation & Modeling principal at Grant Thornton, explained: “In a time of volatility and continued uncertainty in the market, everyone has an interest in informed decision-making and fact-based negotiation that will provide the most stable outcome and lower the chances of later being disputed. Ultimately, Monte Carlo simulations are better suited to delivering the valuations that make that possible.”

While each transaction has unique characteristics, a Monte Carlo simulation is the presumptive choice when structuring, negotiating and valuing earnouts.

Our featured valuation and modeling insights

No Results Found. Please search again using different keywords and/or filters.