As more private businesses begin implementing the new U.S. GAAP standard under ASC 842, Leases (“ASC 842” or “the standard”), many are discovering that they no longer have easy access to the data needed to compute the most common book/tax differences. Prior to implementing ASC 842, many taxpayers have general ledger accounts such as “Deferred Rent” or “Prepaid Rent” that allow visibility into identifying and computing major/book tax differences. However, under ASC 842, those accounts are going away and have been replaced by a right-of-use asset and corresponding lease obligation onto their balance sheet for fiscal years beginning on or after Dec. 15, 2021, for private companies. The standard also requires companies to take a fresh look at how they are treating leases for GAAP purposes. Thus, the standard not only removes the accounts that used to be used to track book/tax differences—it may create new ones.

Most of the dialogue, articles, CPE courses, etc. have concentrated on the GAAP rules and reporting requirements. Also, most software solutions focus on the GAAP requirements. As a result, some of the tax impacts of the new standard have not been fully considered.

The biggest change under the standard for lessees is that lessees are required to recognize an asset and liability for most leases on its balance sheet, which requires completely changing the journal entries used to report and track the lease expense. The standard does not fundamentally change lease accounting from the lessor’s perspective, but there are some changes that require lessors to look to the new GAAP revenue recognition standard under ASC 606, which in certain instances may impact the new revenue recognition rules under the Tax Cuts and Jobs Act (TCJA). Additionally, lessees subject to the IASB standard, IFRS 16, instead of the GAAP standard, must report all leases as finance leases, which may create new book/tax differences on the tax return.

Tracking for historical book/tax differences is gone

As noted above, the journal entries used to track and record the balance sheet and income statement accounts are changing under the new GAAP and IFRS leasing standards, which will create challenges for continuing to identify and compute the common book/tax differences. To offer a better understanding of what is changing, below are some of the most common book/tax differences and a quick summary of some of the new GAAP requirements for operating leases.

Straight-line rents

One of the most common book/tax differences is for rent deductions. Generally, for operating leases, GAAP requires fixed rent payments to be expensed straight-line over the term of the lease, whereas for federal income tax purposes, generally the rules require taxpayers to deduct rents following the payment schedule for most conventional leases.

Under the former GAAP rules for an operating lease, the difference between the actual payments of rent and the straight-line expense were usually recorded in a Deferred Rent or Prepaid Rent account on the balance sheet, which made it relatively easy to identify for tax purposes.

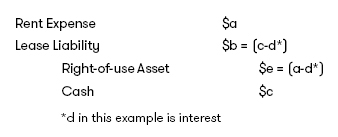

The new GAAP standard requires a lessee to record a right-of-use asset and a lease liability for all leases with a lease term greater than 12 months.1 There is no more Deferred Rent or Prepaid Rent account. Instead, at the commencement of the lease, the lease liability is equal to the present value of the lease payments.2 The initial right-of-use asset is equal to the lease liability plus any initial direct costs minus any lease incentives received plus any payments made by a lessee to the lessor at or before the lease commencement date.3 Therefore, if there are no initial direct costs, lease incentives, or prepayments, the right-of-use asset equals the lease liability. The straight-line expense will be recorded in the income statement, the lease liability will be reduced by the difference between the cash payment and the interest expense on the lease liability, and the amortization of the right-of-use asset is the difference between the straight-line expense and the interest.4

Thus, a typical journal entry will look something like:

For federal income tax purposes, the tax treatment will depend on whether the lease is subject to Section 467 or the general accrual rules under Section 461. In either case, taxpayers usually deduct rent by following the payment schedule for most conventional leases (leases without a separate rent allocation schedule that do not have provisions that alter the benefits and burdens of ownership) without prepayments.5 Thus, in the above journal entry, tax would deduct when the cash is paid rather than following the straight-line GAAP expense.

Many small equipment leases—and some commercial real estate leases—are subject to the general rules under Section 461, which require accrual method taxpayers to deduct rent in the year in which the liability meets the all-events test and economic performance rules. Economic performance for rent is met as the leased property is used, i.e. ratably over the period of time the taxpayer is entitled to the use of the property.6 Therefore, for conventional leases with monthly rent payments, a taxpayer would deduct the rent monthly, while for leases with prepaid rent a taxpayer must spread the deduction ratably over the period of use related to the prepayment.

The Section 467 rules override the general federal income tax rules under Section 461 regardless of whether a taxpayer uses the overall cash or accrual method of accounting—and they often apply to commercial real estate leases and large equipment leases. A Section 467 rental agreement is any rental agreement for the use of tangible property with aggregate payments exceeding $250,000, and under which there are either increasing or decreasing rents and/or there is prepaid or deferred rent. Thus, if a lease agreement has fixed, stepped rents that are not based on the consumer price index (CPI), the lease will be subject to Section 467 if the total payments exceed $250,000.

Note that the definition of prepaid or deferred rent under Section 467 is not as broad as is commonly used in books and records. Historically (prior to ASC 842), a taxpayer may record in its books and records deferred or prepaid rent for any month in which payments do not match the book deduction. However, to have deferred or prepaid rent under Section 467 for federal income tax purposes, the regulations require that the payment schedule in the lease agreement not match the rental allocation schedule in the lease agreement. For example, Treas. Reg. Sec. 1.467-1(c)(3)(ii) provides that a rental agreement has prepaid rent if the cumulative amount of rent payable as of the close of a calendar year exceeds the cumulative amount of rent allocated as of the close of the succeeding calendar year. Thus, there is only prepaid rent under Section 467 if the prepayment in calendar year 1 exceeds the amount of rent allocated cumulatively through calendar year 2.

In computing the rent to be accrued each year under Section 467, rents must be allocated in accordance with the applicable Section 467 rental agreement.7 In most conventional leases, there is no rent allocation schedule separate from the rent payment schedule in the lease. Therefore, in these situations, the lessee generally recognizes an expense in accordance with the rent payment schedule and there is no prepaid or deferred rent under Section 467.8

The regulations can be daunting to tackle, as they first make the reader determine if any of the special rules apply, such as the constant rental accrual method (which applies if the IRS determines that the lease is disqualified long-term lease or a disqualified leaseback because the IRS has determined that the principal purpose for providing increasing or decreasing rent is the avoidance of federal income tax) or the proportional rental accrual method (which applies if there is prepaid or deferred rent, as described above, without adequate interest), even though these rules rarely apply to conventional lease terms. Under Treas. Reg. Sec. 1.467-1(c)(2)(ii), if there is a rent allocation schedule that is different from the rent payment schedule, then the parties follow the rent allocation schedule, provided the special rules do not apply. Generally, parties may create leases with a rent allocation schedule that is different than the payment schedule if the parties are executing tax planning.

Therefore, for conventional leases with fixed, increasing rents, taxpayers generally would follow the cash payment schedule for federal income tax, but would straight-line the expense for GAAP. Taxpayers face a potentially burdensome tracking issue to reconcile the book/tax differences now that the Deferred Rent and Prepaid Rent general ledger accounts are gone.

Lease incentives

The treatment of lease incentives also has long been a source of book/differences. As noted above, lease incentives are included in the right-of-use asset under the new GAAP standard. Thus, the lease incentive is amortized against the lease expense over the life of the lease. For tax purposes, however, a lease incentive is often taxable to the lessee at the commencement of the lease.

Generally, for federal income tax purposes, a lessee has gross income when it receives a lease incentive from the lessor because it has an accession to wealth—unless the facts indicate that the allowance was intended to be spent on real property improvements owned by the landlord.9 Thus, incentives for moving expenses, payments to the lessee’s former landlord to terminate its prior lease, and certain tenant construction allowances owned by the lessee are gross income to the tenant upfront.

The tenant bears the burden of proving it does not have an accession to wealth.10 Whether the improvements are owned by the tenant or the landlord must be determined using tax principles, which generally rely on the benefits and burdens of ownership.11 If the tenant owns the asset, the lease incentive is gross income when the lessee has a fixed right to the income and it is determinable with reasonable accuracy, which is generally near the commencement of the lease.12 The tenant will capitalize the leasehold improvement asset and depreciate for tax purposes when placed in service.

However, there are certain safe harbors, such as Section 110, which allow for the lessee to exclude the incentive from income to the extent it is used to construct real property improvements. If the parties intend for the landlord own the improvement upfront, the lease should either specifically reference language from the Section 110 regulations and/or specifically state that the landlord owns the improvements upfront (not just at the end of the lease). Because the landlord owns the improvements, the lessee should not capitalize and depreciate the improvements that are built or purchased with the eligible allowance.

It can be difficult to qualify for the safe harbor in Section 110. The requirements include:

- The allowance must be spent on qualified long-term real property

- The lease must be for retail space and run for 15 years or less

- The lease must contain language expressly from the regulation (e.g. the “allowance is for the purpose of constructing or improving qualified long-term real property for use in the lessee’s trade or business at the retail space”)

- The lessee must attach an information statement to the tax return in the year the allowance is received

- The lessor must capitalize and depreciate the improvements.13

If the Section 110 safe harbor is not met, taxpayers must rely on case law to determine which party has the benefits and burdens of ownership of the improvements. Generally, the IRS will look for specific language in the lease that indicates the landlord intended to own the improvements upfront.

Thus, incentives such as tenant allowances are a very common book/tax difference. Under the new GAAP standard, taxpayers also face a potentially burdensome tracking issue to reconcile the incentive book/tax differences now that the incentives are buried in the right-of-use asset.

Lease terminations

Another difference is the treatment of payments made by a lessor to an existing tenant to incentivize the tenant to terminate its lease. For federal income tax purposes, an amount paid to terminate or facilitate the termination of an existing agreement does not facilitate the acquisition or creation of another agreement unless the lessor and lessee are renegotiating an existing lease agreement.14 However, if a lessor pays a lessee to terminate an existing lease agreement, the lessor must capitalize the termination payment and amortize over the term of the old lease.15

There also may be differences if the tenant makes a payment to a lessor to terminate a lease. If the lessee makes a payment to the lessor to terminate a lease and does not owe any back rent and is not terminating the lease in order to enter into another lease or to buy the property, the payment is generally deductible as rent.16 However, if the lessee makes a payment for back rent for less than the lessee owes, there may be income that needs to be recognized under Section 108 (income from discharge of indebtedness) or under Section 111 (recovery of tax benefit items). Further, if the lessee is terminating a lease to enter into a new lease or buy the property, then the payment will generally be capitalized and pulled into the new lease or cost of the property.17

Substantial modifications/rent concessions

Normally, substantial changes to lease agreements are somewhat unusual on a large scale, however COVID-19 has caused many rental agreements to be modified. These modifications affect both tenants’ and property owners’ GAAP and tax accounting.

Common changes can take the form of any of these:

- Reduced rent

- Rent forgiveness,

- Extension of lease,

- Deferral of rent payments (during or after lease terms)

- A combination of these things.

GAAP provides specific guidance on whether to treat changes as rent concessions or rent modification. The allowance to account for these as concessions or modifications is dependent on the evidence of an “enforceable right” to the concession (i.e., if the laws in the jurisdiction governing the lease could create a legally enforceable right to a concession). If this enforceable right exists and there are no other terms of the lease that have been changed, the situation can be considered a concession as opposed to a lease modification.

The Financial Accounting Standards Board (FASB) staff recently issued a staff Q&A addressing the accounting for lease concessions related to the effects of the COVID-19 pandemic under ASC 842.18 The FASB staff states that the published guidance on lease modification standards was written with routine lease changes in mind and not for the novel and widespread concessions granted in response to the COVID-19 pandemic. Due to these special circumstances, the staff believes that under both ASC 840 and ASC 842, the entity may elect to treat qualifying lease concessions as if they were based on enforceable rights and obligations and may choose to apply or not to apply modification accounting for the qualifying concession.

Two criteria must be met to be considered a qualifying concession. First, the concession must be related to COVID-19. Second, there cannot be a substantial increase in the lessee’s obligation or the lessor’s rights under the contract. For example, the total payments required by the modified contract must be substantially the same as, or less than, the total payments required by the original contract.

One of the more common lease concessions is a deferral of rent that changes the timing of the rental payments, but not the amount of these payments. The FASB staff noted there could be multiple approaches to accounting for deferrals under both ASC 842 and ASC 840. One approach is to continue to account for the lease as if no deferral has been provided. A lessee should record a payable and a lessor should record a receivable for rental payment deferred. If these criteria are not met, then under ASC 842, the rent concession is a modification. Both lessee and lessor must first determine if a lease modification should be treated as a new lease or as a continuation of the current lease. An entity accounts for a modification that is not considered a separate contract as a continuation of the existing lease and should reassess the lease classification, analyzing all modified terms and conditions and updating all inputs as of the effective date of modification.

There are important tax implications of changes to lease agreements. Treatment of Section 467 and non-Section 467 leases differ. If a change is considered a lease modification under Section 467 it could lead to a change in the remaining lease from being subject to Section 461 to being subject to the rules of Section 467. For example, a substantial modification under Section 467 rental agreement would be considered a new, separate lease from the old agreement. Due to these circumstances, determining what qualifies as a substantial modification is very important, as under a lease modification the categorization of the lease would have to be re-evaluated. A modification is considered substantial only if, based on all the facts and circumstances, the legal rights or obligations that are altered and to the degree to which they are altered are economically substantial.

Typically, for Section 467 leases, the fixed rent for a rental period is the amount of the fixed rent allocated to the rental period under the rental agreement. Therefore, the income or expense is recognized in the period that it is allocated.

Certain modifications to an existing lease could turn a lease that did not have increasing or decreasing rents—and thus was subject to Section 461—into a Section 467 rental agreement due to the uneven rents caused by the rent deferrals. If rents are significantly prepaid or deferred, the taxpayer may be required to use the proportional method of recognition. Certain modifications could trigger the deferred rent provisions, requiring the use of the proportional method under Section 467 instead.

If the leases are not Section 467 leases, then entities must evaluate the recognition rules under Section 451 for income and Section 461 for expense to determine the appropriate timing for recognizing the new payment schedule.

Interest on finance leases

As described above, the treatment of deferred rent, lease incentives and initial direct costs may create new book/tax differences in some circumstances, even though for many leases, there were already differences under the old rules. Another possible new book/tax difference is interest on finance leases.

Under the standard, the initial measurement of the right-of-use asset and lease liability is the same for operating and finance leases, while the expense recognition and amortization of the right-of-use asset differ significantly. Finance leases will reflect a front-loaded expense pattern similar to current capital leases.19 Unlike operating leases, the interest expense on the lease liability and the amortization of the right-of-use asset (generally straight line) will be reflected separately on the income statement. Under the standard (and for IFRS as well), the income statement will include interest expense on the lease. Thus, if any leases were formerly characterized as operating leases for book purposes but are now finance leases for book purposes, the amount of the book/tax differences may change due to the interest computation. This is a particularly notable issue for leases subject to IFRS 16, as all leases are treated as finance leases.

As noted below, it is also important to make sure that the book interest on the finance lease is reversed for leases that are true leases for federal income tax purposes.

Interest limitation under Section 163(j)

A common question business owners ask is how the new interest limitation interacts with the leasing rules. Effective for tax years starting in 2018, Section 163(j) limits the deduction for business interest to the sum of these three amounts:

- Business interest income

- Thirty percent of the taxpayer’s adjusted taxable income for the tax year

- The taxpayer’s floor plan financing interest for the tax year

Any interest not deductible because of the Section 163(j) limitation is carried forward indefinitely (with some restrictions for partnerships).

The IRS and Treasury issued final regulations under Section 163(j) that includes amounts treated as interest under a Section 467 rental agreement in the definition of interest for purposes of the limitation.20 Generally, this type of interest arises with leases that have unconventional terms, such as a lease with a rent holiday that exceeds 24 months, or a lease that specifically provides two separate rent schedules: one that allocates rent to each year of the lease and one that provides for a deferred or prepaid payment schedule that is different than the allocation.

The book interest computed on leases that are finance leases for GAAP (or IFRS) is not interest for federal income tax purposes if the lease is a true lease for tax. (Remember that for operating leases, GAAP only reports rent expense in the income statement, so there will not be interest expense on operating leases.) However, if the lease is a sale/financing for federal income tax purposes, then the purported rent payments would have to be split between interest and payment on the loan. Whether a lease is a sale/financing for tax rather than a true lease depends on the facts and circumstances and does not automatically match the GAAP (or IFRS) treatment.21

Other items to consider

With the standard, renewed attention should also be placed on the following items, if applicable:

- Lease classification: While GAAP defines leases as either operating or finance, the federal income tax rules define leases as either a true lease (also known as: operating lease) or a sale/financing arrangement (somewhat similar to a finance lease). Federal income tax laws list numerous factors to consider when determining the classification of a lease that should be analyzed.

- Sale/leaseback transactions: There are likely book-to-tax adjustments that exist when this transaction occurs as GAAP and tax treatment generally will differ in whether a sale actually occurs and when the resulting gain/loss on the sale gets recognized.

Beyond federal tax

There are a variety of state and foreign tax impacts, including:

- State apportionment for income taxes: The computation of the property factor may be impacted to the extent that the property factor is computed based on the GAAP basis of property if the right-of-use asset is included in plant, property and equipment. Additionally, certain states include a multiple of rent expense incurred for the year in the property factor.

- Franchise and net worth taxes: The new standard may impact the net worth of a company to the extent the tax is based on GAAP net worth due to the inclusion of the right-of-use asset and the lease liability in the balance sheet.

- Personal property or real estate taxes: In jurisdictions that impose property taxes on personal and real property, businesses will need to determine if the right-of-use asset constitutes property subject to the local property tax.

- Sales and use tax: Determine whether any applicable jurisdiction takes the position that a right-of-use asset is the equivalent of a purchase of such an asset from the lessor, thereby resulting in an immediate sales tax imposition on a purchase transaction.

- Foreign income taxes: To the extent that a company operates in foreign jurisdictions that base their local income tax liability on accounting income, the company will need to evaluate the impact of the new lease standard on foreign income tax expense.

- Transfer pricing: Transfer pricing rules may require that related parties reflect an arm’s-length price regardless of what the treatment is for GAAP purposes.

Lessors may have to accelerate income

Under ASC 842, a lessor should allocate the contract consideration to the separate lease and non-lease components in accordance with the transaction price allocation guidance in ASC 606, Revenue from Contracts with Customers.22

Generally, lessors recognize fixed, increasing rents straight-line over the term of the lease under ASC 842. The federal income tax rules are the same under Section 467 for lessors as for lessees, and therefore there will generally be a book/tax difference due to the difference between the book straight-line and the tax payment schedule.

For leases that are not subject to Section 467, the lease income would be subject to Section 451. For accrual basis taxpayers with applicable financial statements (AFS), Section 451(b) generally requires that taxpayers recognize income no later than when it is recognized in their AFS. The final regulations under Treas. Reg. Sec. 1.451-3 illustrate that taxpayers that have an enforceable right to the income accelerated in the AFS under the straight-line method if the contract were cancelled, would have to accelerate the income for federal income tax purposes as well.

Summary

These are some of the most common book/tax differences on operating and finance leases and, as illustrated, taxpayers may have issues going forward with identifying the appropriate book/tax differences due the new GAAP reporting requirements. Additionally, as part of the implementation of ASC 842, a taxpayer may discover that it was not appropriately following the federal income tax rules. In that case, the taxpayer must change an impermissible method of accounting for the treatment of any of these items by filing a Form 3115, Application for Change in Method of Accounting. Certain changes may be eligible under the automatic method change procedures.

For more information, contact:

David Murdock

Partner

David has 19 years of experience in taxation with an emphasis in corporate income tax compliance, income tax provision (ASC 740) and Strategic Federal Tax Services, which include R&D Tax Credit, UNICAP (Inventory Capitalization), Cost Segregation/Fixed Asset Solutions, and comprehensive Credit, Methods and Periods palnning.

San Jose, California

Industries

- Construction & real estate

- Manufacturing, Transportation & Distribution

- Technology, media & telecommunications

- Retail & consumer brands

Service Experience

- Tax

- Corporate Tax

- Strategic Federal Tax

To learn more visit gt.com/tax

1 Paragraph 842-20-25-1 of ASC 842.

2 Paragraph 842-20-30-1 of ASC 842.

3 Paragraph 842-20-30-5 of ASC 842.

4 Paragraphs 842-20-25-6 through 842-20-35-6 of ASC 842.

5 Treas. Reg. Sec. 1.467-1(d)(2)(iii) and (c)(2)(ii).

6 Treas. Reg. Sec. 1.461-4(d)(3).

7 Treas. Reg. Sec. 1.467-1(d)(2)(iii).

8 Treas. Reg. Sec. 1.467-1(c)(2)(ii). See also, Stough v. Commissionner, 144 TC 306 (2015) (under Section 467, taxpayers were required in the year of receipt to include as gross income the entire lump-sum payment made pursuant to the terms of the lease because the lease did not specifically allocate fixed rent to any rental period).

9 Section 61; John B. White, Inc., 55 TC 729 (1965); In re The Elder-Beerman Stores Inc., 97-1 USTC 50,391 (Bankr SD Ohio 1997); Price, 77 TCM 1928 (1999).

10 Id.

11 Id.

12 Section 451.

13 Treas. Reg. Sec. 1.110-1(b) and (c).

14 Treas. Reg. Sec. 1.263(a)-4(e)(1)(ii) and Treas. Reg. Sec. 1.263(a)-4(d)(6)(iii).

15 Treas. Reg. Sec. 1.263(a)-4(d)(7).

16 Section 162.

17 Letter Ruling 9607016.

18 FASB Staff Q&A – Topic 842 and Topic 840: Accounting for Lease Concessions Related to the Effects of the COVID-19 Pandemic.

19 Paragraph 842-20-25-5 of ASC 842.

20 Treas. Reg. Sec. 1.163(j)-1(b)(22)(i)(J).

21 See, for example, Section 7701(e) and a long list of cases including Torres, 88 T.C. 702 (1987).

22 Paragraph 842-10-15-38 of ASC 842.

Tax professional standards statement

This content supports Grant Thornton LLP’s marketing of professional services and is not written tax advice directed at the particular facts and circumstances of any person. If you are interested in the topics presented herein, we encourage you to contact us or an independent tax professional to discuss their potential application to your particular situation. Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein. To the extent this content may be considered to contain written tax advice, any written advice contained in, forwarded with or attached to this content is not intended by Grant Thornton LLP to be used, and cannot be used, by any person for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

The information contained herein is general in nature and is based on authorities that are subject to change. It is not, and should not be construed as, accounting, legal or tax advice provided by Grant Thornton LLP to the reader. This material may not be applicable to, or suitable for, the reader’s specific circumstances or needs and may require consideration of tax and nontax factors not described herein. Contact Grant Thornton LLP or other tax professionals prior to taking any action based upon this information. Changes in tax laws or other factors could affect, on a prospective or retroactive basis, the information contained herein; Grant Thornton LLP assumes no obligation to inform the reader of any such changes. All references to “§,” “Sec.,” or “§” refer to the Internal Revenue Code of 1986, as amended.

More alerts

No Results Found. Please search again using different keywords and/or filters.