The IRS recently published guidance (Notice 2023-17), establishing initial rules for allocating enhanced credit rates for certain types of solar and wind projects under Section 48(e).

Section 48 generally now provides a 30% base credit for a variety of energy projects. The Inflation Reduction Act (IRA) allows increased rates for specific types of projects, including an additional 10% rate for projects in “energy communities” and 10% for domestically sourced projects. The “environmental justice” allocation addressed by Notice 2023-17 provides an increased credit of either 10% or 20% for solar or wind projects in connection with certain low-income communities.

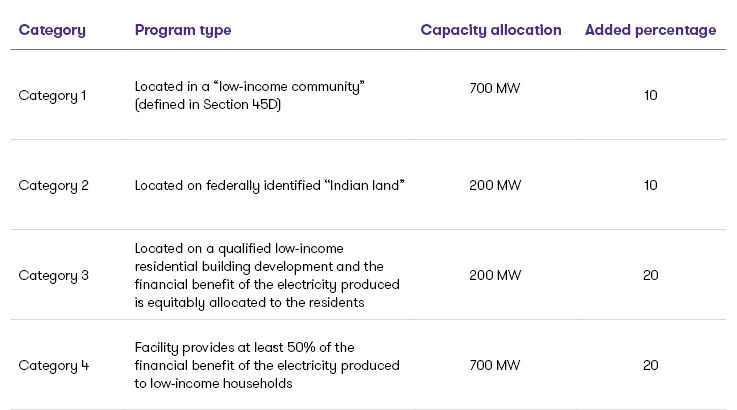

The facilities must have a maximum net production of less than 5 megawatts (MW). Treasury has a limited allocation of only 1.8 gigawatts (GW) worth of projects it can award under the program for calendar years 2023 and 2024, and taxpayers must apply for a portion of the allocation. The notice provides that for 2023, the 1.8 GW capacity limitations will be allocated among the four categories of communities eligible for the low-income community benefit as shown in the chart below.

The guidance does not set the specific application deadlines or provide the application itself. The notice does specify that applications will be accepted in stages in 2023, beginning with a 60-day application window in the third quarter of the year. This first window will accept applications only for Category 3 and Category 4 facilities described above. Category 1 and Category 2 facility applications will be taken at a later point in 2023, yet to be determined.

The application must be submitted by the owner of the project and can only be made with respect to one allocation category. It is not clear whether “owner” in this context refers to the project company that owns the facility or, if a project company is a disregarded entity, the tax owner of the facility.

The Department of Energy (DOE) will be responsible for administrating and evaluating low-income community benefit applications. Unlike the Section 48C program, it does not appear that the DOE will rank qualified projects in order to determine who is funded. Instead, the notice provides that if the total applications for one of the four categories exceed the capacity for such category, then the IRS may use a lottery system or other processes. Conversely, if the capacity in any category is not fully used in 2023, the excess may be reallocated by the IRS to another category to maximize the 2023 allocations. There will be no waitlist for denied applicants, so rejected applicants must reapply the following calendar year to be reconsidered.

The notice does not provide the full criteria for determining whether projects will qualify, but did indicate there will be a focus on facilities that:

- Are owned or developed by community-based organizations and mission-driven entities

- Encourage new market participants

- Provide significant benefits to low-income communities and people excluded from economic opportunities

- Have a higher level of commercial readiness

Detailed information on this criteria is not provided; however, additional details are expected in the coming months.

The property must be placed in service within four years after the date the applicant was notified that the capacity limitation was allocated to the project. Eligible property is considered placed in service in the earlier of the taxable year in which the period for depreciation begins, or the taxable year in which the property is placed in a condition or state of readiness for a specifically assigned function.

Interested entities should carefully review the information contained in Notice 2023-17 and be on the lookout for additional guidance from DOE and Treasury in the coming months.

Contact:

Tax professional standards statement

This content supports Grant Thornton LLP’s marketing of professional services and is not written tax advice directed at the particular facts and circumstances of any person. If you are interested in the topics presented herein, we encourage you to contact us or an independent tax professional to discuss their potential application to your particular situation. Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein. To the extent this content may be considered to contain written tax advice, any written advice contained in, forwarded with or attached to this content is not intended by Grant Thornton LLP to be used, and cannot be used, by any person for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

The information contained herein is general in nature and is based on authorities that are subject to change. It is not, and should not be construed as, accounting, legal or tax advice provided by Grant Thornton LLP to the reader. This material may not be applicable to, or suitable for, the reader’s specific circumstances or needs and may require consideration of tax and nontax factors not described herein. Contact Grant Thornton LLP or other tax professionals prior to taking any action based upon this information. Changes in tax laws or other factors could affect, on a prospective or retroactive basis, the information contained herein; Grant Thornton LLP assumes no obligation to inform the reader of any such changes. All references to “§,” “Sec.,” or “§” refer to the Internal Revenue Code of 1986, as amended.

More tax hot topics

No Results Found. Please search again using different keywords and/or filters.

Share with your network

Share