Professional services firms are facing growing pressure to disclose their ESG metrics. Increasingly, firms need to provide these metrics for regulators, loans, insurance, customers, employees and other business activities.

“Different firms will feel the pressure to different degrees, but all firms will probably start to feel some pressure directly or indirectly,” said Grant Thornton Risk Senior Manager Chris Hanson.

Professional services firms must provide sufficient oversight for tracking and disclosing this information, much like financial records. That means firms need processes and internal controls to ensure the data is complete, accurate and consistent across disclosures. When a regulator inquires about inconsistencies in the reporting of ESG metrics or other issues arise, firms might need to respond with an internal review or investigation.

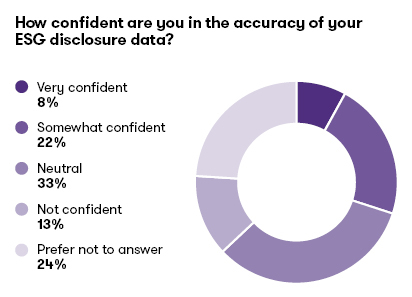

In a recent Grant Thornton webinar about ESG disclosures for professional services, almost 300 attendees answered questions about their organization’s ESG data — and only 8% indicated that they were “very confident” in the accuracy of that data.

As ESG data requirements become more common, and more formalized, firms must be prepared to respond.

Standards to consider

ESG includes a range of topics, which means it can include a range of data. “Industry by industry, organizations have struggled with what metrics or information should be disclosed, and how to establish the appropriate level of validation through internal or external assurance,” Hanson said.

In assessing what ESG disclosures are important for an organization, consider the full range of stakeholders. The resulting priorities will drive the selection of information to disclose. To align information with established norms for disclosure, you can consider standards such as the Global Reporting Initiative, the Sustainability Accounting Standards Board, the Task Force on Climate-related Financial Disclosure (TCFD) and even a proposed SEC rule on Climate-related disclosures.

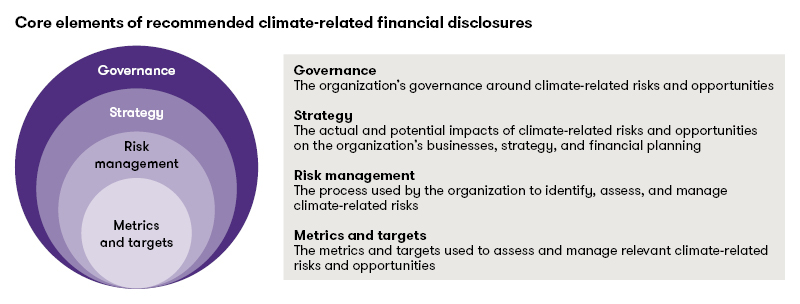

Standards are still evolving, but firms should be putting compliance frameworks in place. In creating such frameworks, organizations need to think broadly about the interplay of board oversight, the organization’s strategic priorities, addressing inherent risks and sharing reliable ESG information. These considerations are part of most guidance from leading international bodies setting standards and putting forth formal frameworks for ESG disclosures. For instance, TCFD recommends four core elements for climate-related financial disclosures.

To start analyzing which ESG data you might need to track and report:

- Define the sources of ESG data

- Identify policies, processes and internal controls that should be in place to assess data quality

- Consider the evolving regulatory framework and case law that could affect a disclosure

- Demonstrate recognition of industry sector priorities for disclosure

Define sources of quality ESG data

ESG data can come from various teams, and some of them might not be accustomed to validation or disclosure.

“For decades, ESG data has had less scrutiny on it. It comes from different parts of the organization, and they might not have much third-party review or internal controls in place,” said Grant Thornton Risk Director Dan Mosher.

Firms can consider established standards to help ensure that, once they determine what information to report, the disclosure’s underlying process and form follows a structure that the marketplace and investment community generally accepts:

Human resources

Consider SASB’s Workforce Diversity and Engagement Disclosure

Human resources can track the percentage of gender and racial/ethnic group representation for executive management, and for all other employees.

Facilities management

Consider the calculation of Scope 2 Greenhouse Gas emissions

The U.S. EPA defines Scope 2 emissions as the indirect Greenhouse Gas emissions associated with the purchase of electricity, steam, heat or cooling.

Travel

Consider the calculation of Scope 3 Greenhouse Gas emissions

Scope 3 emissions are the result of activities from assets not owned or controlled by the reporting organization, but that the organization indirectly impacts in its value chain.

Marketing

Consider the current SEC enforcement stance

If an issuer chooses to speak on climate or ESG — whether in an SEC filing or elsewhere — it must ensure that its statements are not materially false or misleading, or misleading because they omit material information — just as it would when disclosing information in its income statement, balance sheet, or cash flow statement. (Gurbir Grewal, Director, SEC Division of Enforcement, November 8, 2021)

Once a firm establishes the sources for comprehensive and accurate ESG data, it also needs to ensure that it maintains the ongoing quality of that data into the future through monitoring efforts and enhancements to disclosure protocols that will scale with the organization’s growth.

“Think about how much new information you want to capture, to monitor and report on ESG, and then think about what sort of processes and controls are in place to produce reliable information,” Hanson said.

Ensure ongoing quality for ESG data

Firms need to establish policies, processes and internal controls to ensure the quality of their ESG data. Firms also must be able to demonstrate these policies, processes and controls to stakeholders such as their clients, strategic partners, M&A counterparts and possibly regulators. There are several factors to consider:

- Policies and processes for data governance must ensure:

- Provenance of data

- Consistency of data

- Protection of data, from its origin to disclosure

- Internal controls must establish data completeness and accuracy:

- Segregation of duties between the underlying data and the ESG reporting, to make sure the data is evaluated by someone other than who prepares it

- Reconciliation to other data sources

- Audit trails

- The type of assurance of disclosures that is appropriate:

- The skills sets and approaches used by any third parties providing assurance

- Forms of assurance that may range in the depth, breadth and rigor of testing and coverage

For an organization just starting its journey for rigorously supported ESG information, there are alternatives for establishing some baseline information as a starting point. “Even if there isn't good data governance in place, there are a lot of data analytics techniques that can help triangulate information between different sources,” Mosher said.

For example, look at checking your data on diversity, equity and inclusion (DE&I) against data that you reported to the U.S. Equal Employment Opportunity Commission. If your Greenhouse Gas emission data relies on proxy information such as the total square footage of your firm’s rented facilities, reconcile these inputs to your leases to make it an accurate and well-sourced calculation.

Service firms need to have a full understanding of ESG data to identify and mitigate pitfalls in data accuracy and completeness.

Prepare for an enhanced level of scrutiny

“If you're going to put something into your financial statements, it had better be accurate — both from a disclosure standpoint and any statement about risks,” Mosher said. “That’s also the case for ESG.”

Beyond collecting data to meet specific requirements, services firms that want to claim a leading role in corporate responsibility need to make sure they have the data to back it up. “Look at how you travel,” Hanson suggested. “Because we're talking about jet fuel use, taking multiple legs is going to have a bigger carbon footprint than a direct flight. Are you willing to trade off costs on a direct flight versus the carbon footprint, and then how do you track that information?”

Inaccurate or insufficient data can lead to accusations of false advertising or other legal claims, in addition to regulatory violations. “The accuracy with which you are advertising yourself as a socially responsible corporate citizen can get you in trouble, from a legal standpoint,” Mosher said. Service firms need to set up protocols that vet ESG information in marketing content against ESG source data in a manner similar to financial disclosures.

As ESG expectations continue to evolve on multiple fronts, scrutiny of ESG data will continue to rise, and can require an investigation if there are allegations of misrepresentation. Make sure that your firm has quality data that is ready to meet this scrutiny, whether it’s to satisfy regulations or support your reputation.

Featured ESG insights

No Results Found. Please search again using different keywords and/or filters.

Share with your network

Share