The SEC issued a Final Rule, Management’s Discussion and Analysis, Selected Financial Data, and Supplementary Financial Information, to modernize, simplify, and enhance certain Regulation S-K disclosure requirements. Among other things, the amendments eliminate Regulation S-K, Item 301, Selected financial data; streamline the requirements in Item 302, Supplementary financial information; and update certain requirements in Item 303, Management’s discussion and analysis of financial condition and results of operations.

Grant Thornton insight

Some stakeholders who commented on the proposed rule expressed the need for additional disclosure requirements relating to environmental, social, or governance issues (ESG) and sustainability matters. Given the SEC’s principles-based approach to MD&A, the Final Rule does not adopt new requirements specific to ESG or sustainability matters. However, registrants are encouraged to include such disclosures in their filings to the extent they are deemed material information.

MD&A

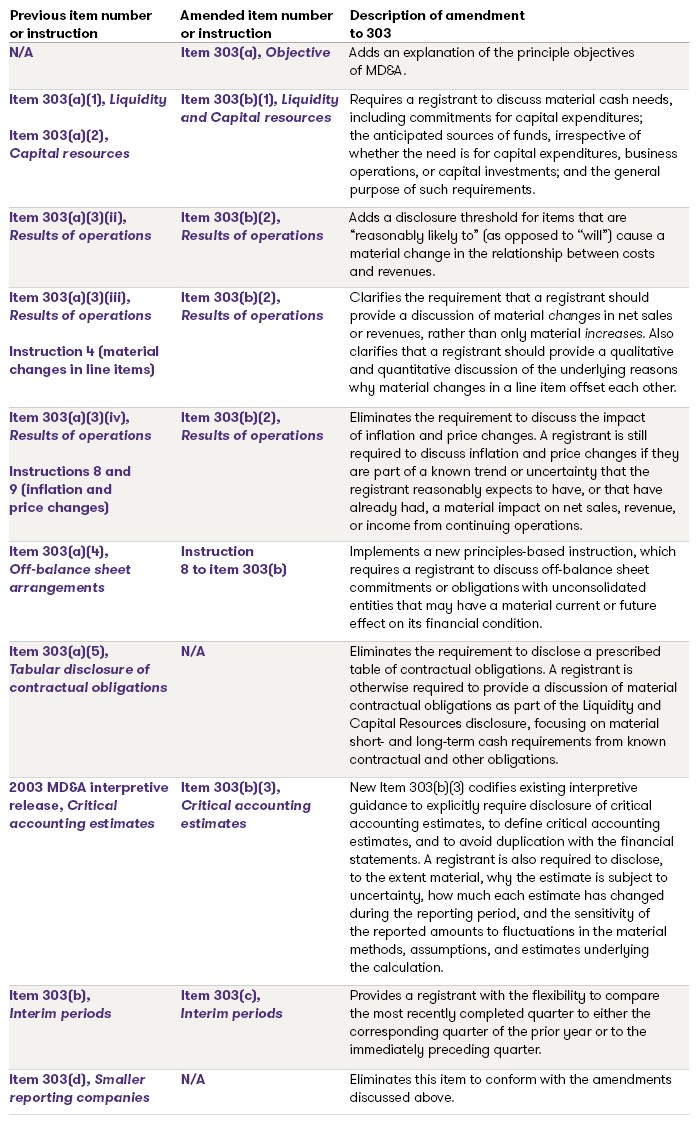

The Final Rule expands the principles-based nature of the disclosure framework in Management’s Discussion and Analysis (MD&A) and codifies existing Commission guidance on this topic. The amendments further streamline disclosures and reduce redundancy between MD&A and existing U.S. GAAP disclosure requirements. See a summary of the amendments in the table below.

Other amendments

Although the Final Rule eliminates Item 301, a registrant is encouraged to continue to consider whether tabular disclosure may be appropriate in an introductory or overview section, including disclosures that demonstrate material trends.

Under the amendments to Item 302(a), a registrant is no longer required to provide two years of selected quarterly financial data. Rather, a registrant should use the principles-based approach to reflect any material retrospective changes to previously presented quarterly financial information. Item 302(a), as amended, applies beginning with the first filing on Form 10-K after a registrant’s initial registration statement.

The Final Rule adopts parallel changes to certain financial disclosures provided by foreign private issuers, as well as conforming amendments to Forms 20-F and 40-F.

Compliance dates

The Final Rule is effective 30 days after publication in the Federal Register.

Registrants are required to apply the amended rules in their first fiscal year ending on or after 210 days after the Final Rule is published in the Federal Register (the mandatory compliance date). The amended rules apply to a registration statement and prospectus that, on its initial filing date, include financial statements for a period ending on or after the mandatory compliance date.

Contacts:

© 2020 Grant Thornton LLP, U.S. member firm of Grant Thornton International Ltd. All rights reserved.

This Grant Thornton LLP bulletin provides information and comments on current accounting issues and developments. It is not a comprehensive analysis of the subject matter covered and is not intended to provide accounting or other advice or guidance with respect to the matters addressed in the bulletin. All relevant facts and circumstances, including the pertinent authoritative literature, need to be considered to arrive at conclusions that comply with matters addressed in this bulletin. For additional information on topics covered in this bulletin, contact your Grant Thornton LLP professional.

Audit insights and technical guidance

No Results Found. Please search again using different keywords and/or filters.