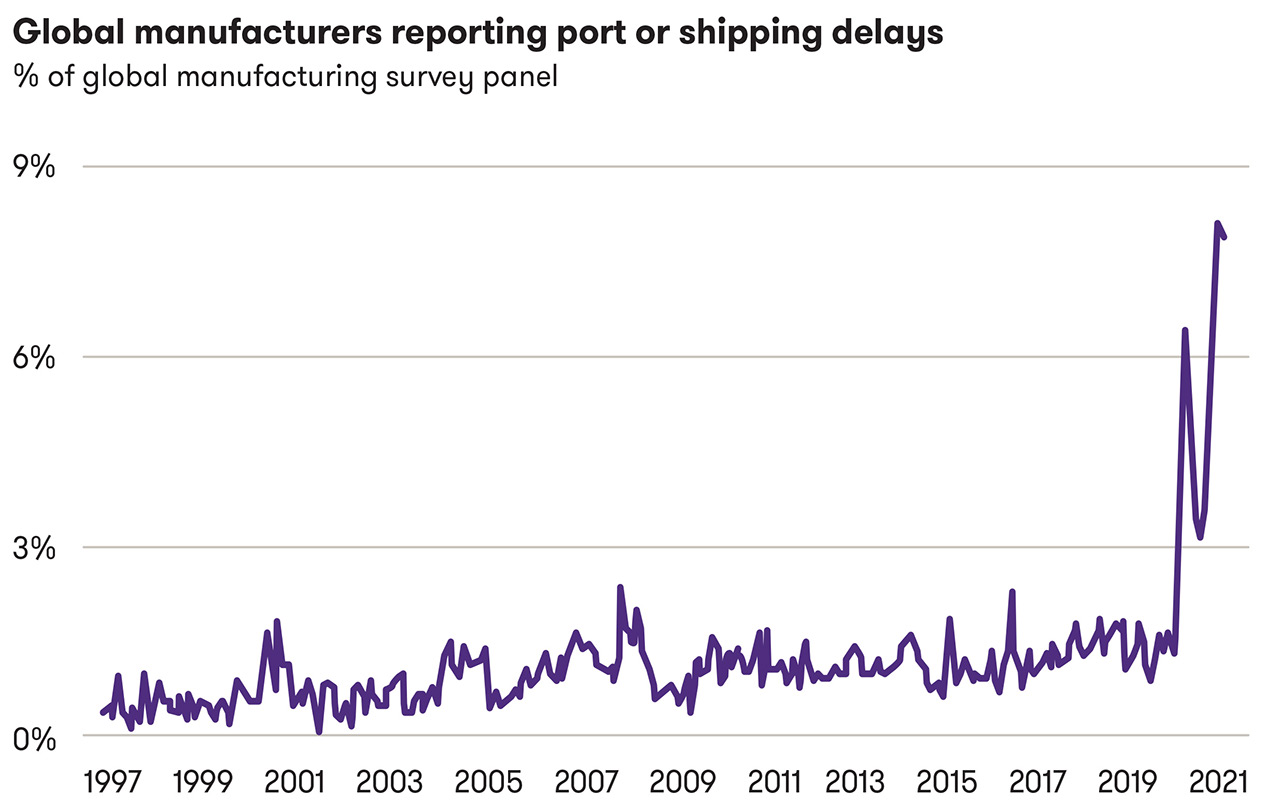

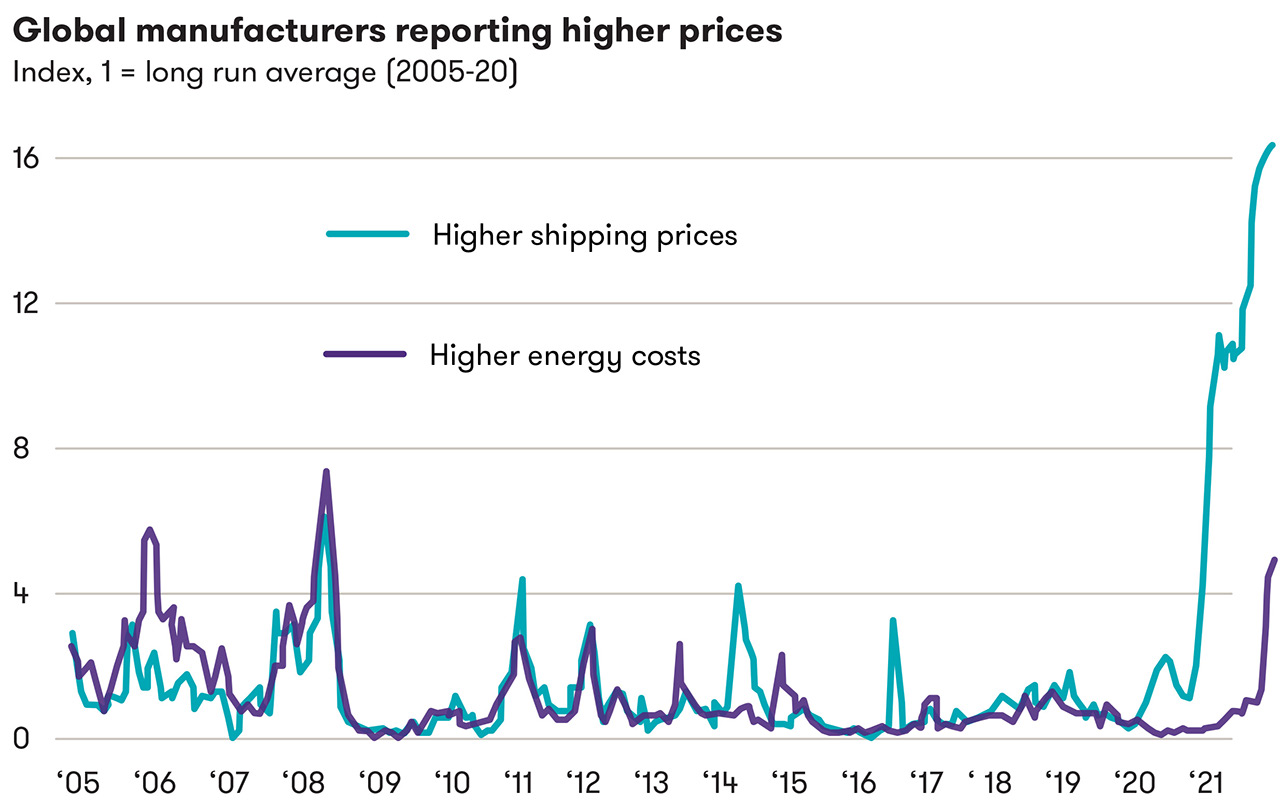

Manufacturers, distributors and retailers have been weathering a perfect storm of global supply chain disruptions that created a crisis on almost every front. Production, distribution, and workforces have all been impacted — and prices at the shelf are facing the most significant inflationary pressures in recent history.

“The current global supply chain crisis is arguably one of the deepest and farthest-reaching operational disruptions we’ve seen in decades,” Grant Thornton National Sourcing and Supply Chain Transformation Leader Ben YoKell said.

“From an operational perspective, it’s even more persistent and damaging than September 11, 2001, or the Los Angeles/Long Beach Longshoreman’s strike of 2012,” YoKell added. Import shipping costs, manufacturing lead times and product availability are now outside of historical norms.

Slowdowns in every sector have exacerbated each other, driving higher costs upstream and downstream. Grant Thornton National Managing Principal for Manufacturing Robert Hersh said, “What we’re seeing now is that those external disruptions are trickling into the plant, to the shop floor. They’re affecting the flow of materials, workforce, technologies and processes required to maintain business continuity and customer service — and ultimately, they’re affecting the pricing itself.”

It’s been hard for anyone to escape the downward pull of the pandemic. Now, manufacturers are looking at how to avoid such disruptions in the future while still offering high levels of service at low costs in spite of rising inflation.

Did manufacturers get too lean?

The U.S. manufacturing industry has spent decades trimming its business models for better efficiency, cost, customer service and speed to market.

Now, the magnitude of the pandemic-induced supply chain disruption has forced manufacturers to rapidly re-examine their supply chain strategy, inventory levels, distribution routes to market and operational resiliency. The imperative is both financial and operational; board rooms across the country are asking about supply chain risk management, supplier diversification, and alternative global manufacturing or sourcing strategies, with some CXOs openly challenging decades of accepted practice in low-cost sourcing, just-in-time inventories, and lean approaches.

But YoKell cautions these executives against overreaction and wholesale departure from the pursuit of efficient and effective processes and practices.

“Our industry needs to be more sophisticated, agile, adaptive and risk-measured in its deployment of capital.”

“There will always be a tremendous amount of value from process efficiency, waste elimination, lead time reduction and extremely careful inventory management,” YoKell said. “But our industry needs to be more sophisticated, agile, adaptive and risk-measured in its deployment of capital. Financial, technological and human capital must enable the business and brand strategy, with maximized returns that account for the downsides of disruption.”

The challenge for most companies is in having the right data, metrics, tools and processes to make holistic business decisions that balance customer service, cost to serve, speed to market, working capital, and risk resilience. How can manufacturers adapt, to better deploy capital and prepare for future risks?

Rethink the manufacturing model

“Where we really had problems through this crisis is with the just-in-time inventory model.”

“Where we really had problems through this crisis is with the just-in-time inventory model,” Hersh said. “I think there’s an optimal level of inventory in any system, and I think we let that inventory system get a little too lean.”

However, manufacturers need to do more than increase inventory levels, as that will have working capital, cash flow, and obsolesce downsides along with increased warehousing and storage requirements. Right now, distribution real estate is also facing historical shortages as economic activity rebounds and direct-to-consumer ecommerce fulfillment centers have exploded to keep up with the rapid shift away from brick-and-mortar shopping.

Beyond rethinking the global manufacturing strategy and near-shoring or re-shoring key components, materials, and production, Hersh said that more manufacturers are turning to distributed manufacturing. Manufacturers that pivot to be closer to customer consumption points can be more nimble about late-stage differentiation and customization. They can also get products to market more efficiently, with material requirements landing closer to the point of sale with less risk disruption.

“We’re entering a period where an OEM can design a product all digitally, and it’s a question of how you distribute those digital designs all over the world to bring the supply chain together,” Hersh said. For instance, manufacturers can send digital designs to 3D printers that are close enough for the customer to pick up the product right away. “I’m working with a client that’s doing that right now,” Hersh said. “It’s that type of creative thinking, about how to apply automation and other new technology, where I think we’re going to see the next positive disruptive innovations, after we solve these supply chain issues.”

This technology-enabled model extends far beyond the floor, into aspects of advanced forecasting and planning. “Manufacturing 4.0, Integrated Business Planning and predictive approaches are not new to the buzz word bingo of supply chain management,” YoKell said. “But, as a result of the pandemic, we are now seeing more material investment in integrated planning platforms, advanced forecasting and predictive technologies. We’re also seeing the daily application of AI/ML, RPA, IoT-based sensing and cloud-based workflow enablement.”

As manufacturers digitize the way of work, from the shop floor through the office functions, they achieve faster and more effective scenario planning. This increases business agility and reduces the internal latency of adjusting to changes in both demand and supply.

Rethink the workforce

New technologies and new manufacturing models require new recruiting models. “This is not your grandfather’s manufacturing industry anymore,” Hersh said.

As manufacturers adopt new technologies to stay competitive, they need to recruit new skills and consider:

- Moving CapEx projects to the people (labor source), not the other way around

- Using economic development zones and state and local incentives to fund new investments and/or offset costs of right-locating facilities to the labor pools

- Finding markets newly rededicated to technical and trade skill development

- Cultivating training, documentation, quality, safety and working conditions

- Aligning with environmental, social and governance (ESG) initiatives on corporate social responsibility, which today’s modern workforce is increasingly attuned to as part of choosing a future employer

“We need to get other people involved in the manufacturing realm that don’t look like the wrench turners of the old days,” Hersh said. New technologies will require more data analysts and machine learning experts to automate processes and make them more efficient. That’s part of why manufacturers need to recruit from a broader base of people, including more women.

“That can mean finding new recruitment markets, cultivating training and even doing things that align business strategy with the bigger picture of corporate social responsibility,” YoKell said.

From production and distribution to business processes and workforce, the manufacturing industry is changing. The manufacturers that grow and succeed will be the ones that effectively adapt. “The key theme here is ‘efficient, effective and scalable,’” YoKell said.

Our manufacturing featured industry insights

No Results Found. Please search again using different keywords and/or filters.

Share with your network

Share