Looking beyond upcoming disclosure requirements, finance leaders consider their strategic ESG priorities

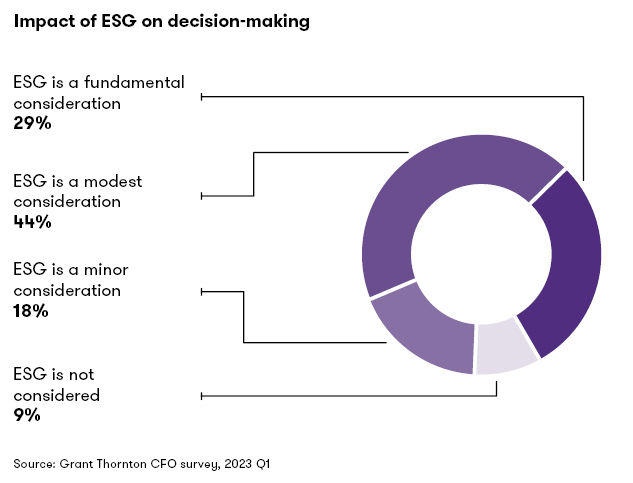

CFOs are good at following the rules. That’s why it isn’t a surprise that with the SEC expected to issue climate-related disclosure requirements soon, CFOs are prioritizing environmental, social and governance (ESG) initiatives. In Grant Thornton LLP’s Q1 2023 CFO survey, 73% said they either moderately or fundamentally consider ESG topics in their organization’s decision-making.

The Corporate Sustainability Reporting Directive passed in the European Union (EU) will add further ESG compliance requirements for thousands of public and private companies that have revenue or operations in the EU.

“This is an all-CFO issue,” said Elizabeth Sloan, Grant Thornton Managing Director of ESG & Sustainability Services. “The expanding global and potential US disclosure requirements mean organizations will need consistent data for regular reporting at the ready. Right now, all CFOs should be looking through their organization and making sure they have a strong and repeatable data collection process in place.”

“Right now, all CFOs should be looking through their organization and making sure they have a strong and repeatable process in place.”

While tracking and reporting ESG data in preparation for required disclosures is imperative, CFOs are prioritizing ESG programming for other reasons, too. Evolving stakeholder expectations and the impact of ESG data on other business goals are prompting CFOs to dedicate resources toward advancing their ESG initiatives.

Moving forward, CFOs will need to balance seeing the “forest” — long-term ESG goals and their impact on broader organizational goals — with the “trees” of determining the specific initiatives that will help them not only meet upcoming disclosure requirements, but build a successful, meaningful ESG program that bolsters their organizational identity with trackable results.

Related Resources

ARTICLE

REPORT

CFOs’ ESG priorities go beyond disclosure requirements

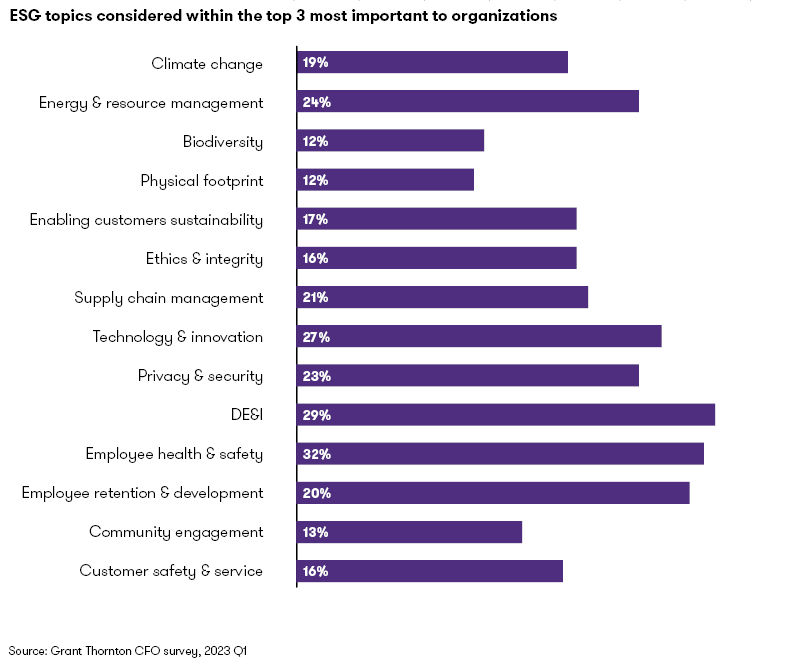

All eyes are on the SEC's upcoming climate-related disclosure requirements — but the latest CFO survey shows financial leaders are thinking beyond climate in their ESG strategies. Less than one fifth (19%) of CFOs ranked climate change as a top ESG topic for their organization. About a third considered employee health and safety (32%) and diversity, equity and inclusion (DE&I) (29%) in their top three priorities, and over a quarter included technology and innovation (27%) as an important element of their implementation plan.

CFOs also noted the benefits of incorporating ESG initiatives into their business practices — particularly, its role in safeguarding against reputational risk and associated financial consequences. Today, brand reputation means more than good PR — it is a major factor in a company’s sustained valuation. More than half (56%) of survey respondents said improving the reputation of their brand is a benefit of an enhanced ESG program. Other benefits ranked highly include enhanced trust among stakeholders (45%) and attracting and retaining talent (38%).

CFOs are attaching the benefit of ESG to their reputation likely because they believe it’s a priority for their stakeholders, too, as stakeholder groups that play a role in advancing ESG are shifting across organizations. In the latest survey, 39% of CFOs said customers are one of the stakeholder groups pushing them to enhance their ESG programs. That’s up from 28% who said the same in Q3 2021. In this survey, CFOs put customers only behind leadership (44%) and employees (43%) as the stakeholder groups motivating their ESG program. That is likely because the younger generation is taking up more space as both employees and customers, prompting organizations to take ESG topics that group cares care about more seriously.

Looking ahead to the next generation

The oldest members of Gen Z turn 26 this year. They’re participating in the economy as customers and investors, and in coming years, they’re expected to make up roughly a third of the workforce.

So, when the majority of CFOs acknowledge brand reputation as a benefit of incorporating ESG initiatives into their organization, they’re looking past check-the-box activities such as an annual report. Embedding ESG into their culture, brand and even supply chain — and tracking it — will become increasingly important to the next generation.

“The next generation — as consumers, employees and investors — is looking at organizations holistically. Not just as a business that provides a service, product or job opportunities, but as an organization that embodies their values in the way that they operate day-to-day. And they’re looking to align themselves with those values,” said Suha Gillani, director of ESG & Sustainability at Grant Thornton.

“The next generation — as consumers, employees and investors — is looking at organizations holistically. Not just as a business that provides a service, product or job opportunities, but as an organization that embodies their values in the way that they operate day-to-day. And they’re looking to align themselves with those values.”

DE&I is another key consideration as organizations plan ESG strategies for the long-term. It was the top topic that CFOs said was most often discussed with their board, at 34%.

One reason DE&I continues to remain at the forefront of conversations is the recent increase in layoffs in some industries. For companies that have begun hiring with a DE&I focus, the current and potential upcoming rounds of layoffs could hinder their DE&I goals, particularly if they lose that talent to the common practice of last in, first out. Now, with many industries facing a tight labor market, it will take work to recruit those hires back. Thoughtfully embedding DE&I and ESG practices into talent decisions, from hiring to talent cuts, will be imperative moving forward and can help organizations learn from past experiences.

As organizations consider how to include DE&I in their ESG strategies, they should recognize they can’t be everything to everyone, but instead focus on where they’ll be able to see the most impact.

“Every organization is set up differently, and progress against DE&I strategies can be driven by leadership, employees, vendors and more,” Gillani said. “Think of the business lines where you can have the most impact while strengthening your business and then put dollars to that, track progress against that in the short run instead of stretching resources too thin across multiple initiatives.”

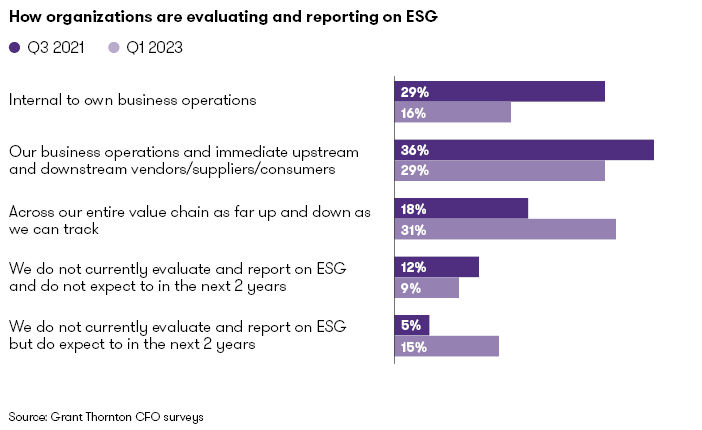

This sentiment ties into another finding from the CFO survey — that organizations are increasingly tracking their ESG progress across the supply chain. In fact, 31% of CFOs said they evaluate and report on ESG initiatives across the entire value chain as far up and down as they can track — up from 18% when the question was last asked in Q3 2021.

So, if CFOs are recognizing the importance of ESG topics that go beyond regulation disclosures — how are they strategizing what to prioritize, and how are they reporting on and tracking that data?

Reporting: An opportunity to showcase strengths

No one wants to scramble for a deadline. If that’s how an organization managed their ESG reporting up until this point, it will be nearly impossible to put their best foot forward when sharing progress with stakeholders, as well as for mandatory disclosures to the SEC.

“Many managers don’t have a built-in process for ESG reporting the same way they would for performing something like cash reconciliation. When it’s an all-hands-on-deck situation, there are likely reporting issues and mistakes in the data,” Sloan said. “ESG reporting needs to be built with the same rigor as their regular financial reporting. If not, then it continually becomes a burden — and they lose their own effectiveness and efficiency in collecting data.”

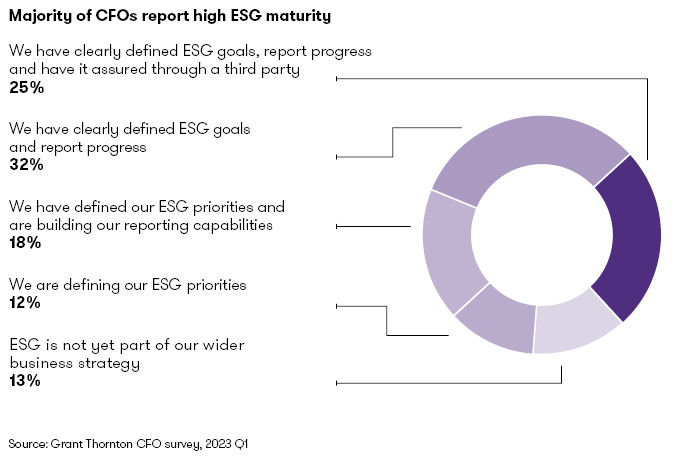

Luckily, the majority of CFOs surveyed — 57% — report they have clear ESG goals and are at least building their reporting capabilities against these goals. And they’re taking action to strengthen their ESG programs in various ways — from identifying priorities through a materiality assessment (48%), developing a gap analysis against current disclosure requirements (47%), conducting assurance readiness over reported metrics (34%) and obtaining independent assurance (31%). Just 18% of CFOs aren’t doing any of these things. And to prepare to report on new ESG-related regulatory requirements, such as CSRD and the proposed SEC rule, more than half (51%) are getting their reported data validated by a third party, with 27% using a CPA firm.

Still, CFOs foresee some challenges when it comes to ESG reporting. Nearly half said ensuring accurate and reliable data collection (46%) and maintaining compliance across multiple jurisdictions with different reporting requirements (44%) will be challenges as their organization increases its focus on ESG initiatives. But rather than consider ESG reporting daunting, leaders can view it as an opportunity to show their strengths — using information they already have.

“When we see CFOs prioritizing employee health and safety, tech, DE&I... it shouldn’t be daunting to think about extracting that information,” Sloan said. “Your organization likely already has much of this data. Wouldn’t it be great if you could reliably and consistently come up with it, have it assured and show your stakeholders what a great job you’re doing?”

With a focus on the big picture, organizations can make their ESG program work in their benefit. As CFOs guide their organizations through ESG strategy, operations and reporting, they have the opportunity to take their ESG programming beyond compliance and use their data to tell their stories, engage their stakeholders and improve their double bottom line.

Featured ESG insights

No Results Found. Please search again using different keywords and/or filters.

Share with your network

Share