Key items for directors to review

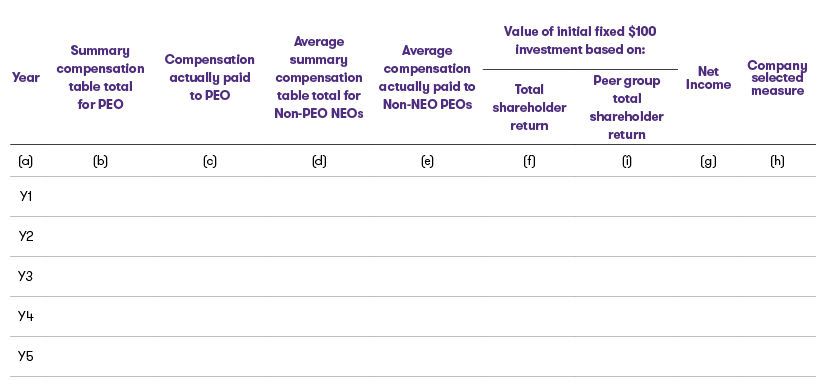

Back on Aug. 25, 2022, the SEC released final rules for the pay versus performance disclosure originally required in the Dodd-Frank Wall Street Reform and Consumer Protection Act. The disclosure requirement, which will be effective for fiscal years ending on or after Dec. 16, 2022, will take the form of an additional table that will be included in future proxy statements. Companies will need to report compensation and financial calculations that have not been previously required, including compensation actually paid, an average of compensation for non-CEO named executive officers, company and peer group total shareholder return (TSR), and a company-selected measure that represents the strongest link between organizational pay and performance.

While companies, their outside counsel, and external advisors should review the final 233-page regulation in full detail, there are several key areas that compensation committees and boards will need to monitor.

Pay and company performance

The most surprising difference between the SEC’s originally proposed regulations in 2015 and the final rules is a new compensation actually paid calculation. Though salaries and cash bonuses will be valued the same for both the summary compensation table and compensation actually paid columns, the methodology for calculating equity and pension values will be vastly different.

Unlike the summary compensation table, which only reports the value of equity awards at the time they are granted, compensation actually paid will measure the combined value of (i) awards granted during the most recent year and (ii) the change in value of awards granted in previous years.

Directors should closely monitor the change in value of previously granted equity and how it compares to both the summary compensation table and overall organizational performance. Should any real or perceived disconnects exist, directors should be prepared to disclose the rationale for the differences and offer additional guidance and support for the current compensation philosophy and structure.

Company-selected measures

A second item from the final regulations that surprised many outside observers is the inclusion of a company-selected measure that represents the “most important financial performance measures used by the registrant to link executive compensation actually paid during the fiscal year to company performance.” Companies have a wide degree of latitude to select generally accepted accounting principles (GAAP) or non-GAAP measures, and may include multiple company-selected measures in the table as long as they are not “misleading or obscure the required information.” In addition to the quantitative values required in the company-selected measure column, companies will need to describe the relationship between their selected metric and compensation actually paid.

Compensation committees should consider the most appropriate company-selected measure to use and how that measure relates to their existing compensation plans. Our early discussions with clients indicate that the most heavily weighted metric in an annual or long-term incentive plan may be an appropriate starting point. Companies should carefully consider selecting any metrics that are not already included in an incentive plan, and prepare to provide substantial disclosure for why their company-selected measure is not part of the existing compensation plan should they choose to do so.

Start early

The finalized pay versus performance regulations require significantly more calculations and disclosures than the proposed rules issued in 2015. The SEC has, however, exempted emerging growth companies, registered investment companies, and foreign private issuers from the new rules, and provided smaller reporting companies reduced requirements, such as not requiring peer group TSR or a company-selected measure. The SEC has also implemented a two-year transition period during which initial filings will only require the three prior fiscal years, increasing over time to the required five years.

Given that disclosures will be required in 2023 proxy statements, boards should encourage management to start calculations early to ensure they identify the data points, processes, and analyses that will be needed for their pay versus performance tables.

Contacts:

Partner, Human Capital Services

Grant Thornton Advisors LLC

Eric Gonzaga is a Principal and practice leader for the Human Capital Services (HCS) group in Minneapolis.

Minneapolis, Minnesota

Industries

- Healthcare

- Technology

- Not-for-profit & Higher Education

Service Experience

- Tax Services

- Human Capital Services

Trending topics

No Results Found. Please search again using different keywords and/or filters.

Share with your network

Share