Determining value when a sale is a creditor’s best recovery option

For creditors dealing with bankrupt debtors, selling the debtor or its assets is sometimes a more efficient way to realize cash than working through a reorganization plan. Sales through Section 363 of the Bankruptcy Code are attractive to debtors and investors due to the expedited nature of the court process and the ability of a buyer to purchase assets free and clear of any liens and encumbrances. Section 363 sales may discourage some interested parties that do not want to compete in an auction or cannot move quickly. However, the process may encourage buyers who are familiar with an industry, have completed due diligence (or can do so quickly) or are ready to close with limited contingencies. To determine whether a sale or reorganization is the better option, the value of the debtor is critical.

Approaches to Business Valuation

No single formula can be used to determine the value of every business in every situation. Therefore, a number of generally accepted valuation methods have been developed. The right approach in a given situation depends on the purpose of the valuation, type of business being valued, available data and other factors. Following are the three most generally accepted valuation approaches.

Income Approach

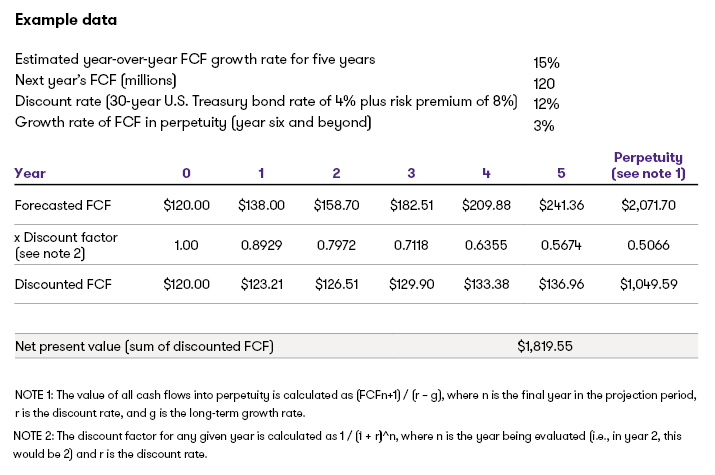

Discounted cash flow (DCF) method. This method determines value based on the company’s projected future cash flows and tends to be more appropriate when future financial results are expected to be different from current results. The indicated value is determined by discounting future cash flows or free cash flows (FCFs) to their present worth using a discount rate that reflects both the current market rate of return and the risks inherent to the specific investment.

In its simplest form, the discount rate represents the rate of return an informed investor would expect to receive on an investment in the business, given the degree of risk inherent to that investment. Factors considered in developing the discount rate include the nature of the business and its outlook at the valuation date, the risks involved, and the stability of earnings. The discount rate can be the sum of the risk-free rate and a risk premium. The risk-free rate is the return that an investor could obtain from an investment with no risk to principal recovery, where such return is normally equivalent to the yield to maturity of long-term U.S. Treasury bonds. The risk premium is the additional return received or expected in exchange for the perceived risk of the investment. The riskier that the investment is perceived to be, the higher the risk premium.

- Capitalization of earnings method. This method develops an indicated value based on the company’s historic earnings. This method tends to be more appropriate when a company’s current financial results are indicative of its future results. The indicated value is determined by dividing a historical benefit stream by a capitalization rate. Depending on the history of the company, it may be appropriate to use only the most current earnings or a weighted average of historical earnings for a number of years.

Market Approach

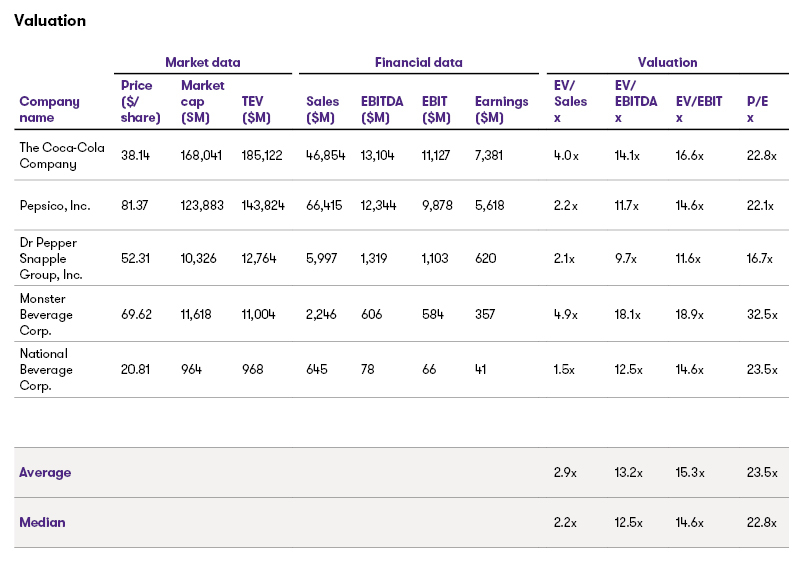

- Comparable transaction method. This method reviews recent transactions in the industry that are like the transaction under consideration and identifies one or more key valuation parameters. That is, are the companies in those recent transactions being valued as a multiple of revenue, profitability (e.g., EBITDA), or some other parameter? Once the key valuation parameters are determined, examine the multiples within those parameters in a series of transactions and then value the company or transaction using the relevant parameters.

- Comparable public company method. Another valuation method starts with the value of comparable public companies (typically in the same industry) and derives one or more multiples based on net income (often referred to as the price/earnings ratio), revenue, EBITDA, or other pertinent parameters. Because of differences between the business being valued and the comparable companies, several adjustments are often considered. Examples of such adjustments may include, among others, a discount for the smaller size typical of the target business or a premium for obtaining control of the business.

Asset-Based Approach

In a limited number of situations, a company’s worth can be estimated by determining the net value of its underlying assets. This approach consists of the adjusted book value method, liquidation value method, and replacement cost method.

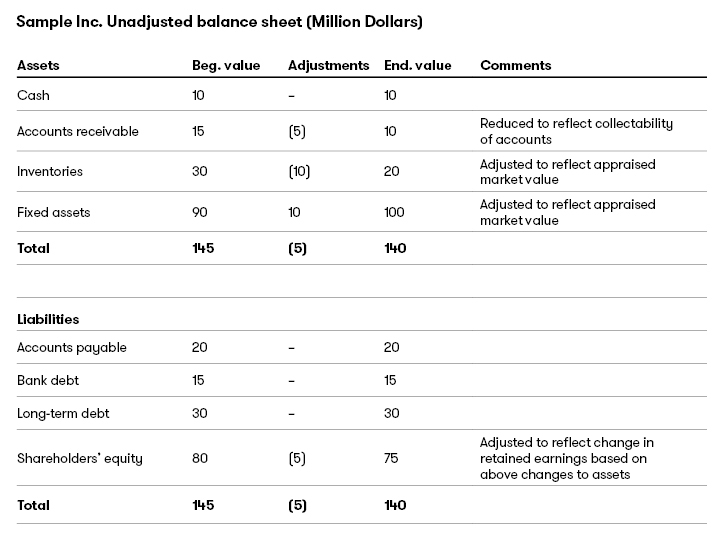

- Adjusted book value method. This method involves adjusting the company’s assets as reported on the company’s books to their realizable values to determine the value of the company. The net value of all the assets and liabilities would be comparable to market value.

- Liquidation value method. This method involves discounting the net proceeds from liquidating the company’s assets and paying off its liabilities to determine the residual value of the company. The adjusted book value is further adjusted to factor in the expected recovery in a liquidation scenario (typically much lower due to the short time frame available to dispose of the assets), as well as the costs of liquidation, which might include broker fees, trustee or receiver fees (if applicable), and other costs associated with disbursing the assets to purchasers. Liquidation values are typically divided into two categories: orderly liquidation values (OLV) and forced liquidation (FLV) or fire sale values. An orderly liquidation value assumes an orderly sale process in which a seller can take a reasonable amount of time (typically 3 to 12 months) to sell its assets to the highest bidder through appropriate sales channels. A forced liquidation value assumes a forced-sale auction with limited time to market and sell the assets. Recoveries in a forced liquidation scenario are typically much lower than those of an orderly liquidation.

- Replacement cost method. This approach determines value based on the dollar amount necessary to reproduce the business enterprise’s tangible and intangible assets and liabilities as part of an on-going business.

The valuation approach employed by potential acquirers in a Section 363 sale will typically involve some combination of these methods. The value of the resulting bids will be influenced by other factors such as, whether the business is being sold as a going concern, the liabilities that may or may not be assumed, whether the acquirer is a financial or strategic buyer, and the nature and conditions of the initial or “stalking horse” bid. Some of the benefits of being a stalking horse bidder include:

- more time to do due diligence

- ability to establish basic terms and conditions for the transaction

- set timeline (subject to court adjustment) for an auction and eventual closing

- ability to receive a break-up fee and/or expense reimbursement if another party is the successful bidder

- and provide input on bidding process.

Negotiation and competitive positioning will also play a key role in determining the ultimate value of a business in a 363 sale. For example, if a bidder wants to acquire a business as a going concern and wishes to retain the existing employees and contracts, there may be an opportunity to increase the perceived value of the offer by assuming priority employee claims and contract cure amounts that other buyers may not be willing to assume.

Each valuation approach requires judgment in its application. Regardless of the valuation methods that are used, value ultimately comes down to what a particular buyer is willing to pay for the specific business and/or underlying assets being evaluated.

Contacts:

Our featured advisory services insights

No Results Found. Please search again using different keywords and/or filters.

Share with your network

Share