Implementation of the “Pillar 2” global minimum tax is gaining traction around the world and will have a significant impact on U.S. multinational enterprises (MNEs) over the next several years.

The Organisation for Economic Co-operation and Development (OECD) has been working toward a global transformation of international tax rules for years. The recent release of Pillar 2 guidance and implementing legislation in several jurisdictions finally gives MNEs crucial new insight into how the rules will operate in practice. The regime generally seeks to impose a 15% minimum tax on the earnings of certain multinational groups with annual revenues of 750 million euros or more. For these MNEs, Pillar 2 threatens to upend core aspects of international tax planning, affecting everything from intercompany financing to transfer pricing.

Despite the important progress toward implementation, key questions remain. There are outstanding technical issues that must be resolved, and there is uncertainty surrounding the outlook and timing for implementation in various jurisdictions. Nonetheless, MNEs should be considering the impact on planning, especially long-term investments in supply chains, intellectual property agreements, and research and development activities. This article will discuss the latest guidance, the outlook for implementation, important unresolved issues, and the potential impact on tax planning.

Background

In October 2021, over 135 countries and jurisdictions comprising the OECD’s Inclusive Framework preliminarily approved a two-pillar plan to reform international taxation rules. Pillar 1 of the plan deals with the allocation of taxing rights based on sales into a country and covers a more limited number of taxpayers—generally only companies with a global turnover above 20 billion euros and a profit margin above 10%. The Global Anti-Base Erosion (GloBE) rules under Pillar 2, on the other hand, generally seek to impose a 15% minimum tax on the earnings of multinational groups with revenues of at least 750 million euros.

Pillar 2 is made up of three interlocking rules: the income inclusion rule (IIR), the undertaxed payment rule (UTPR), and the qualified domestic minimum top-up tax (QDMTT). The IIR imposes a top-up tax at the parent entity level that effectively allows countries to “top up” the tax on earnings of foreign subsidiaries with effective rates below 15%.

The UTPR will generally deny deductions with respect to members of a group with an effective rate below 15% that are not otherwise subject to an IIR. However, countries will be allowed to impose a QDMTT that will take precedence over either an IIR or UTPR. It will effectively “top-up” the tax on domestic entities to 15% to prevent another country’s IIR or UTPR from capturing the revenue.

The OECD has provided guidance on the implementation and operation of the rules in several important tranches:

- Pillar Two model rules released in December of 2021 with initial guidance on the scope of the rules and the application of the IIR and UTPR with an ambitious timeline of domestic implementation of the IIR in 2023 and the UTPR in 2024.

- Consultation documents and additional guidance released in December 2022—including a document on safe harbors and penalty relief that provides relief for MNEs in the initial years by setting up a proposed framework for the future development of two safe harbors for applicable MNEs and a transitional penalty relief regime.

- Long-awaited administrative guidance on Pillar 2, released in February 2023, provides clarifications on several relevant items—including establishing that a QDMTT takes precedence over controlled foreign company (CFC) rules and outlining the rules for allocating a taxpayer’s global intangible low-taxed income (GILTI) as a CFC tax to the relevant tax per jurisdiction.

Safe harbors

The OECD’s December 2022 guidance provides a framework for both a transitional and permanent safe harbor in response to stakeholder comments and requests. The transitional safe harbor identifies lower-risk jurisdictions through the application of three quantitative tests taking information primarily from a business’s country-by-country report (CbCR). On the other hand, the permanent safe harbor, if implemented, would act as a longer-term simplified calculation for applicable jurisdictions.

An MNE that qualifies with respect to one or more jurisdictions is still subject to the full GLoBE Rules in respect to jurisdictions that do not qualify for the safe harbors and must still comply with the group-wide GloBE requirements (i.e., prepare and file its GloBE information return). To qualify, both safe harbors require a tested jurisdiction to meet one of three testing requirements: a de minimis test, effective tax rate (ETR) test, or a routine profits test. Under the guidance, a “tested jurisdiction” is defined as jurisdictions in which constituent entities of an MNE are located.

Transitional CbCR safe harbor

The OECD notes that the purpose of the transition period is to provide relief to MNE groups in respect of the GloBE compliance obligations. The transitional safe harbor applies only where the MNE group prepares its CbCR using qualified financial statements. It applies for fiscal years beginning on or before Dec. 31, 2026, and ending before July 1, 2028. This would allow for up to three fiscal years of relief for most MNEs (two fiscal years for the UTPR).

Generally, if an MNE with a tested jurisdiction qualifies based on one of the three tests, then the top-up tax (i.e, qualified IIR, UTPR, or QDMTT) for such jurisdiction is deemed to be zero and treated as low-risk. However, the guidance notes that the safe harbor does not apply in certain cases where the CbCR does not provide a reliable indication of the MNE group. The three tests are as follows:

- De minimis test: The total revenue and profit before income tax as reflected in the CbCR of a jurisdiction is less than 10 million euros; and the CbCR profit before income tax is less than 1 million euros.

- ETR test: The ETR of the jurisdiction is equal to or greater than the “transition rate” provided for the corresponding fiscal year:

- 15% for fiscal years beginning in 2023 and 2024

- 16% for fiscal years beginning in 2025

- 17% for fiscal years beginning in 2026

- Routine profits test: The jurisdiction’s substance-based income exclusion amount, as calculated under the GloBE rules, is equal to or greater than its profit or loss before income tax.

The OECD explains that special rules and exclusions apply for certain entities and groups, including joint ventures and tax-neutral ultimate parent entities.

In addition, if an MNE group has not applied the transitional safe harbor in a jurisdiction for a year it is subject to the GloBE Rules, the MNE group cannot qualify for the transitional safe harbor for that jurisdiction in a subsequent year. However, this rule does not apply in circumstances where an MNE group does not have constituent entities in a jurisdiction.

Permanent safe harbor

The OECD has also provided guidance for a potential “simplified calculations” safe harbor. If such a safe harbor is agreed upon, it would reduce the number of complex computations and adjustments a constituent entity is required to make for purposes of computing an IIR or UTPR under Pillar 2.

For a constituent entity to qualify for the simplified calculations for a jurisdiction, it must satisfy the three quantitative tests listed above (routine profits, ETR, and de minimis). However, unlike the transitional safe harbor rules, a tested jurisdiction qualifies for the permanent safe harbor by applying the GloBE rules using simplified income, revenue and tax calculations (as opposed to using CbCR data).

GILTI as a CFC tax

The OECD released highly anticipated administrative guidance in February 2023 that includes clarification on the allocation of taxes arising under blended CFC regimes. The guidance on CFC regimes appears specifically designed to address the treatment of GILTI.

The guidance explicitly cites GILTI as an example of such blended CFC tax regime, commonly references GILTI within the provided examples, and provides that GILTI is an acceptable CFC tax under the GloBE rules. The treatment of GILTI and CFC tax taxes is applicable only for a limited time, however, for fiscal years beginning on or before Dec. 31, 2025. It will be re-evaluated for fiscal years that end after June 30, 2027.

Grant Thornton Insight:

The guidance will essentially respect GILTI as somewhat equivalent to an IIR for a two-year interim period, despite the fact that its effective rate is currently less than 15% and it is not applied on a country-by-country basis. The OECD guidance provides detailed rules for allocating GILTI among CFCs in different jurisdictions.

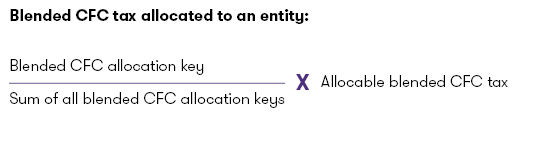

In order to allocate a blended CFC tax from a constituent entity owner to the individual constituent entities, the OECD states that the allocable blended CFC tax is the amount of tax liability incurred by the constituent entity-owner under the blended CFC tax regime. See below:

The OECD’s administrative guidance also clarifies that income tax expense attributable to the QDMTT of a jurisdiction will be included in the computation of the GloBE jurisdictional ETR for that jurisdiction only if the blended CFC tax regime allows a foreign tax credit (FTC) for the QDMTT on the same terms as any other creditable covered tax. This corresponds to additional clarification provided elsewhere in the administrative guidance stating that a QDMTT is computed without regard to CFC taxes and as a result prioritizing the QDMTT before any top-up under the IIR, UTPR, or CFC tax.

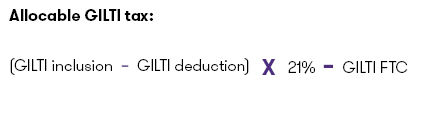

In the case of GILTI and in the absence of a domestic loss, the allocable blended CFC tax and blended CFC allocation key are computed as:

As a result, GILTI taxes are only allocated to jurisdictions with an ETR of less than 13.125% (as computed under the GloBE rules) and ultimately imposes less top-up tax under Pillar 2. The U.S. Treasury Department welcomed the clear guidance on the interaction of GILTI and Pillar 2 via the blended CFC allocation approach. This allocation approach provides Congress an opportunity to amend GILTI to make the regime an equivalent of Pillar 2’s IIR.

Grant Thornton Insight:

The guidance provides some initial favorable results for the U.S., but important issues remain unresolved. It is not clear the extent to which U.S. tax credits will be exempt from the effective tax rate calculation. If not, credits could potentially reduce effective tax rates below 15% and allow other countries to impose their IIRs and UTPRs on U.S. companies.

Pillar 2 offers a general exception for refundable tax credits, and the new guidance includes in this exception several U.S. tax credits that are monetized using tax equity structures. But the guidance is silent on the energy tax credits that became transferable under the Inflation Reduction Act (IRA). It is also unclear how GILTI may be treated after 2026. The transition period potentially gives the U.S. time to implement legislation that aligns more closely with Pillar 2, but legislative efforts remain contentious (discussed more below).

The outlook is also complicated by future changes already built into the tax code. The Section 250 deduction for GILTI purposes is automatically set to decrease from 50% to 21.875% after Dec. 31, 2025. This would increase the effective GILTI rate to 15% after the foreign tax credit haircut, which would better align it with Pillar 2 rules.

But legislation would be needed to truly impose GILTI on a country-by-country basis. More importantly, if the U.S. fails to enact a QDMTT, other countries would be able to capture revenue from U.S. entities with their IIRs and UTPR that a QDMTT would otherwise keep in the U.S.

Jurisdictional updates

Although portions of Pillar 2 are intended to be implemented in domestic law starting in 2023, the OECD’s model rules are, in fact, a guideline for members of the Inclusive Framework to follow. Thus, each jurisdiction within the Inclusive Framework must enact conforming Pillar 2 rules into its local legislation before MNEs will need to apply the rules.

South Korea is the furthest along it the legislative process, having approved domestic legislation providing that both an IIR and UTPR will be effective for fiscal years beginning on or after Jan. 1, 2024. The United Kingdom, the European Union, and Japan have each also made significant strides toward implementation, and other jurisdictions throughout the inclusive framework continue to develop draft legislation, budgets, and additional informative pieces of data. Below are a few key jurisdictions and their recent notable developments:

- South Korea: Domestic legislation has been approved providing that both an IIR and UTPR will be effective for fiscal years beginning on or after Jan. 1, 2024

- European Union: Formally adopted the EU minimum tax directive on Dec. 15, 2022, and provides that member states shall transpose the directive into their domestic law by Dec. 31, 2023. The deal required unanimous agreement and represents a major breakthrough toward implementation and overcoming objections from resistant countries like Hungary and Poland. There are still hurdles ahead, however. The agreement among ambassadors of EU member states in the Committee of Permanent Representatives is to advise the EU Council to adopt the Pillar 2 directive.

- Sweden: Released a white paper proposal concerning Pillar 2 on Feb. 7, 2023, following the adoption of the EU Directive.

- Japan: Released draft legislation on the IIR on Feb. 3, 2023, and provides that the UTPR and QDMTT will not be addressed until Japan’s 2024 tax reform at the earliest.

- Switzerland: Swiss Parliament approved a constitutional amendment to implement the Pillar 2 rules on Dec. 16, 2022. The proposal is now subject to public vote in the summer of 2023.

- United Kingdom: Implementation of an IIR and QDMTT is scheduled for 2024 after draft Pillar 2 legislation was issued in the summer of 2022.

- United States: Implementation of Pillar 2 in the U.S. remains stalled. The Biden administration had hoped to amend international tax rules as part of the IRA in order to implement Pillar 2 in the U.S. Ultimately, those efforts failed, and the White House now faces a Republican-controlled House that has been sharply critical of the global tax agreement. It will be very difficult for legislation to advance over the next 18 months, and the 2024 election may prove critical to whether legislation is possible in 2025. Ultimately, the prospects of double tax on U.S. multinationals and revenue leakage if the rest of the world moves toward implementation could create tremendous pressure for lawmakers to implement changes in the U.S.

Next steps

The Pillar 2 rules will continue to evolve as the OECD releases guidance and member countries enact implementing legislation. But the process appears to be gaining momentum and companies should consider the rules as part of any long-term planning for international investments and tax structuring. Arrangements and investments that appear tax efficient now, particularly those involving low-tax jurisdictions, could quickly become inefficient as the GloBE rules come online. MNEs should follow implementation developments closely and consider modeling out potential scenarios.

For more information, contact:

National Managing Partner,

Washington National Tax Office and International Tax Solutions

Grant Thornton Advisors LLC

David leads the firm's International Tax practice, which focuses on global tax planning, cross border merger and acquisition structuring, and working with global organizations in a variety of other international tax areas.

Washington DC, Washington DC

Industries

- Manufacturing, Transportation & Distribution

- Technology

- Retail & Consumer Brands

Service Experience

- Tax Services

- International Tax

Washington National Tax Office

Partner, Tax Services

Grant Thornton Advisors LLC

Cory Perry is a Grant Thornton partner and Pillar Two leader, advising multinational companies on global tax reform, compliance, modeling, and M&A.

Washington DC, Washington DC

Industries

- Technology

- Manufacturing, Transportation & Distribution

- Private Equity

Service Experience

- Tax Services

Tax professional standards statement

This content supports Grant Thornton LLP’s marketing of professional services and is not written tax advice directed at the particular facts and circumstances of any person. If you are interested in the topics presented herein, we encourage you to contact us or an independent tax professional to discuss their potential application to your particular situation.

Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein. To the extent this content may be considered to contain written tax advice, any written advice contained in, forwarded with or attached to this content is not intended by Grant Thornton LLP to be used, and cannot be used, by any person for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

The information contained herein is general in nature and is based on authorities that are subject to change. It is not, and should not be construed as, accounting, legal or tax advice provided by Grant Thornton LLP to the reader. This material may not be applicable to, or suitable for, the reader’s specific circumstances or needs and may require consideration of tax and nontax factors not described herein. Contact Grant Thornton LLP or other tax professionals prior to taking any action based upon this information.

Changes in tax laws or other factors could affect, on a prospective or retroactive basis, the information contained herein; Grant Thornton LLP assumes no obligation to inform the reader of any such changes. All references to “§,” “Sec.,” or “§” refer to the Internal Revenue Code of 1986, as amended.

Trending topics

Share with your network

Share