Here’s what new rules mean for insurers and policyholders

Florida market regulators continue to make sweeping changes to create a more mutually advantageous atmosphere for both insurers and insureds. Their goal is to increase the supply of available insurance, leading to stabilized insurance rates as well as reducing the burden of the taxpayer-backed plan and bolstering the insureds’ confidence.

Reducing insurers’ costs

Florida is known to be a an overly litigious state with respect to insurance. Florida’s insurance regulators estimate homeowner claims account for 9% of all claims in the U.S., but 79% of all insurance litigation. Florida has now eliminated one-way attorney fees. Now, if an insurer and an insured end up in court and the insured wins, the insurer does not need to pay for the insured’s legal fees. This move by regulators should drastically reduce the insurance companies’ costs. Other helpful moves for insurance companies include:

Prohibition of Assignment of Benefits (AOB). AOB has left the door open to fraud as opportunistic contractors and restoration firms have been known to inflate claims and charge for unnecessary work, or work not performed, often without the knowledge of the insured.

Bad-faith claim elimination. Regulators eliminated the insured’s ability to file a bad-faith claim based solely on the appraisal award or acceptance of judgment. The goal of this change is to prevent the rampant excess cost insurers incur to defend against baseless bad-faith claims. Legal fees for insurers are much higher for civil remedy notices than for breach of contract claims. This leads insurers to often settle. These settlements are in addition to the losses already incurred.

Mandatory arbitration permitted. Insurers may now include mandatory binding arbitration provisions within their policies so long as they offer a premium credit and a policy without this provision. Note that mediation must first occur, and this feature must be a separate endorsement from the policy. New policies may have this feature that, if utilized, would reduce the insurers’ costs and expedite the claims process.

Claims, the insurer’s process and the insureds’ responsibility

In addition to observing new guidance on bad-faith claims and arbitration, insurance firms have new standards to uphold. Many of these regulations should speed the claims process. If a claim is filed, insurers now have one week to acknowledge they received the claim. They also only have one week to begin an investigation after they receive proof of a loss. From there, if a physical inspection is necessary, they have 30 days to complete the inspection (down from 45 days).

If a policyholder is seeking estimates on remediation, they must show the insurer within a week of production of such an estimate. Lastly, and most importantly, insurers must pay, or deny, a claim within two months of the close of the investigation, one month earlier than last year’s standard.

Regulators will be holding insurers accountable. Insurers are required to record:

- All claim communication

- Any proof of loss received

- Any insurer’s request for info

- Any claim-related inspections

- Any estimates generated by the insurer

- The insurer’s payment or denial of claim

In addition, the insurers must disclose to regulators the number of claims opened and closed each month, the number of pending claims each month, and the number of claims using alternative dispute resolution.

Policyholders also have a new role to play. They must file a claim within one year of an incident, down from two years. There are many storms, as well as other drivers of claims, in Florida. The goal of this change is to help insurers more accurately determine the cause and extent of a claim. Delaying a claim can reduce the chances of payment because the insurer may be unsure of the cause of damage. Requiring more timely filing of claims should help claims get adjusted more promptly and reduce potential litigation.

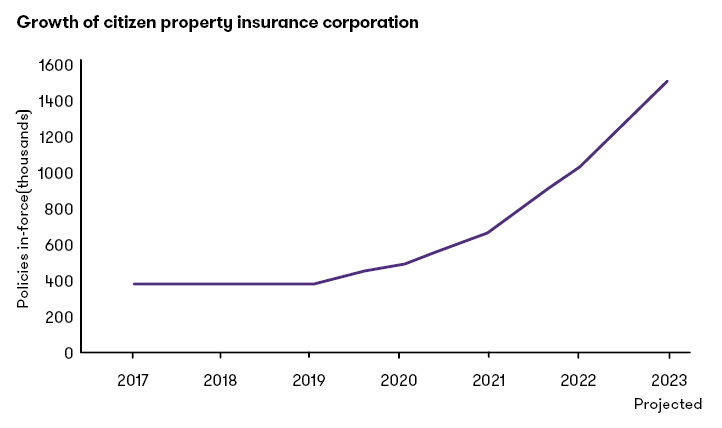

Citizens Property Insurance Corporation

Citizens Insurance was created by the state of Florida as an “insurer of last resort” to provide policies where no comparable private-market option existed. Since inception, it has swelled to be the largest property insurer in the state. Citizens is funded by policyholder premiums, but Florida law also requires that Citizens must have Floridians pay assessments if it experiences a deficit such as in the wake of devastating weather. While Citizens aims to guarantee everyone has access to insurance, the public insurance could leave taxpayers on the hook for billions of dollars.

To counteract this exponential growth, new policy eligibility requirements have been put in place. Private-market premiums for comparable plans must be 20% greater than that offered by Citizens to be eligible for a policy. This is an increase of five percentage points. This comes with a push to make Citizens rates more actuarially sound instead of merely competing with the market. The legislation outlines rate increases occurring for Citizens policies until they reach status.

Additionally, personal residents must hold flood insurance covered by another insurer to qualify for a Citizens policy. These measures are an attempt to curtail the taxpayers’ increasing exposure to risk, create a more competitively priced market and reestablish Citizens as a residual market only for use when insurance is not available in the private market.

Creation of Florida Optional Reinsurance Assistance Program (FOR A)

Reinsurance is essentially “insurance for insurance companies.” It helps insurance firms continue to write policies and protects them in extreme situations, such as hurricanes. Unfortunately, many reinsurers have been exiting the Florida market, which pushes insurers to make a choice: raise rates or exit as well. The state created FORA for the 2023 hurricane season. This optional reinsurance program can act as a backstop for insurers and incentivize them to stay in the Florida market or return.

How will this affect my business and/or home?

Property tax relief for homeowners

For those that suffered damages from Hurricanes Ian and Nicole that left their homes uninhabitable, the state is providing tax refunds on ad valorem property taxes and is extending the suspension of payments of certain taxes and assessments on such properties.

More competitive pricing

By allowing primary insurance carriers to purchase reinsurance (i.e., insurance for insurance companies) from the newly established FORA Fund at a reasonable price, the state has opened the door for primary carriers to enter or re-enter the Florida insurance market. Added competition in the market should promote more competitive pricing on homeowners and commercial property insurance.

Faster claim payments

Insurers must now acknowledge receipt and review submitted claims within seven calendar days of receipt. Within 60 days of receipt, an insurer must pay or deny a claim or a portion of a claim along with reasonable explanation should a claim be denied.

Changes to attorney fees

The elimination of certain attorney fees that incentivize law firms to pursue litigation on your claims with insurance carriers will likely lead to a drop-off in litigation. It will be important for you to take an active role in the handling of your claim and work with counsel and your insurance company representatives to understand the details of your claim and come to the optimal resolution.

Assignment of benefits

You as a property owner (residential or commercial) will no longer be able to assign rights to third parties (i.e., contractors, electricians, etc.) to file claims and receive payments for work done on your property. All claim activity from submission to payment will be your responsibility.

As a business or homeowner, what should I do?

Talk to an independent agent

Agents should be well-versed in the state of the property and casualty insurance market and the impact this legislation will have for their clients. Lean on their expertise to guide you in finding the optimal coverage for your needs, and do not be afraid to get opinions from multiple agents.

Obtain several quotes

Some insurers are intentionally quoting at excessively high rates to deter new business. They are happy to take it on, however, for exorbitant prices. Make sure to obtain multiple quotes to avoid paying excessive premiums when a better offer might be out there.

Understand your coverage

Knowing the intricacies of your coverage will save you from any surprises in the event of a claim. When signing on with a new insurer or even if renewing with your current provider, be sure to comb through the policy details (i.e., binding arbitration clauses, policy exclusions, coverage limits, etc.) For example, if you opt for the minimal level of coverage, the amount you are entitled to recover from your insurer after a covered loss would be unlikely to meet the replacement cost value of your home or business.

Protect yourself from floods

Flood and storm surge damage are not typically covered under a standard homeowners or commercial property insurance policy, while wind damage normally is. In a hurricane-prone geography, having separate flood coverage is vital to protecting your home or business.

Trending topics

No Results Found. Please search again using different keywords and/or filters.

Share with your network

Share