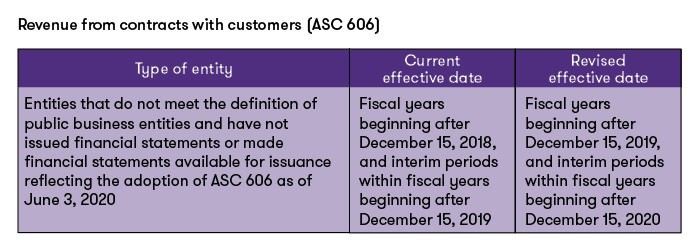

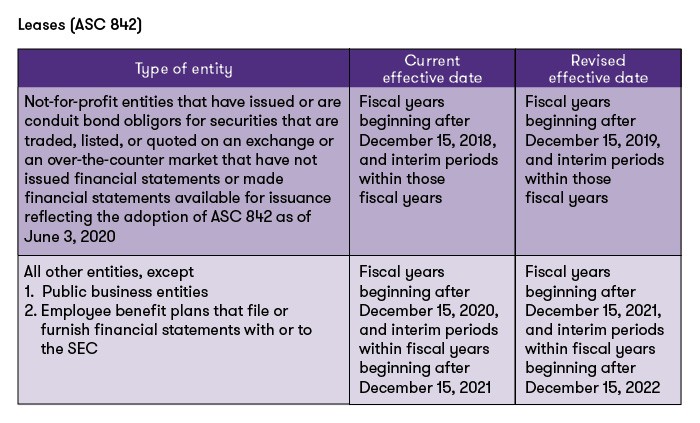

On June 3, the FASB issued Accounting Standards Update 2020-05, Effective Dates for Certain Entities, to defer for certain entities the effective dates for the revenue and leasing standards.

The following tables summarize the revisions to the effective dates. Entities eligible for deferral may still early adopt these standards. The ASU is immediately effective as of June 3, the date of issuance.

References to financial statements in the tables below refer to GAAP-compliant financial statements, which is a widely understood term and includes a full set of disclosures.

Definition

Public business entity

As defined in the Master Glossary in the FASB’s Codification, a public business entity is a business entity meeting any one of the criteria below. Neither a not-for-profit entity nor an employee benefit plan is a business entity:

- It is required by the U.S. Securities and Exchange Commission (SEC) to file or furnish financial statements, or does file or furnish financial statements (including voluntary filers), with the SEC (including other entities whose financial statements or financial information are required to be or are included in a filing).

- It is required by the Securities Exchange Act of 1934 (the Act), as amended, or rules or regulations promulgated under the Act, to file or furnish financial statements with a regulatory agency other than the SEC.

- It is required to file or furnish financial statements with a foreign or domestic regulatory agency in preparation for the sale of or for purposes of issuing securities that are not subject to contractual restrictions on transfer.

- It has issued, or is a conduit bond obligor for, securities that are traded, listed, or quoted on an exchange or an over-the-counter market.

- It has one or more securities that are not subject to contractual restrictions on transfer, and it is required by law, contract, or regulation to prepare U.S. GAAP financial statements (including notes) and make them publicly available on a periodic basis (for example, interim or annual periods). An entity must meet both of these conditions to meet this criterion.

An entity may meet the definition of a public business entity solely because its financial statements or financial information is included in another entity’s filing with the SEC. In that case, the entity is only a public business entity for purposes of financial statements that are filed or furnished with the SEC.

Contact:

© 2021 Grant Thornton LLP, U.S. member firm of Grant Thornton International Ltd. All rights reserved.

This Grant Thornton LLP bulletin provides information and comments on SEC reporting issues and developments. It is not a comprehensive analysis of the subject matter covered and is not intended to provide accounting or other advice or guidance with respect to the matters addressed in the bulletin. All relevant facts and circumstances, including the pertinent authoritative literature, need to be considered to arrive at conclusions that comply with matters addressed in this bulletin.

For additional information on topics covered in this bulletin, contact your Grant Thornton LLP professional.

Audit insights and technical guidance

No Results Found. Please search again using different keywords and/or filters.