However, GILTI ‘high-tax exclusion’ proposal could redefine it if OK’d

The IRS released final (T.D. 9866) and proposed (REG-101828-19) regulations on June 14 addressing a variety of topics including global intangible low-taxed income (GILTI), foreign tax credits, the treatment of domestic partnerships for purposes of determining Subpart F income of a partner, and a so-called “GILTI high-tax exclusion.” The final regulations afford much needed certainty to taxpayers, but were largely upstaged by the proposed GILTI high-tax exclusion that could redefine the GILTI paradigm.

GILTI, enacted under Section 951A, is a crucial component of the international tax system as revised by the Tax Cuts and Jobs Act (TCJA). The final GILTI regulations generally retain the approach and structure of the proposed regulations (REG-104390-18) released in September. The proposed regulations provided taxpayers with guidance in a number of areas, including application of Section 951A to consolidated groups and computational rules addressing tested income and qualified business asset investment. For previous Grant Thornton coverage of the proposed regulations under Section 951A click here.

The regulations also finalize proposed rules under Sections 78, 861 and 965, which were released last November as part of an extensive guidance package to implement changes to the foreign tax credit regime made by the TCJA. For previous Grant Thornton coverage of the foreign tax credit proposed regulations click here.

Although the final regulations retain the approach and structure of the proposed regulations, taxpayers should carefully consider some of the notable revisions, including:

- An overhaul of the treatment of domestic partnerships for purposes of determining GILTI income of a partner

- A number of modifications to the anti-abuse provisions, including changes to the scope

- Basis adjustments for “used tested losses” required under the proposed regulations were not adopted

- Several clarifications that were made with respect to coordination rules between Subpart F and GILTI

Concurrently released proposed regulations could dramatically change the international tax landscape. If finalized, the GILTI high-tax exclusion would have a substantial impact on taxpayers. In essence, it would allow controlled foreign corporations (CFCs) to exclude tested income subject to a “high” effective rate of tax. In many cases, this could alleviate the need to rely on foreign tax credits to eliminate incremental tax on GILTI, and may significantly reduce the income tax labilities of taxpayers subject to foreign tax credit limitations. But this relief is unavailable until the proposed rules are final. The proposed regulations would also apply aggregate treatment to domestic partnerships for purposes of Section 951, effectively treating them as foreign partnerships for purposes of determining income inclusions of domestic partners.

The final GILTI rules are complex and are retroactively applicable to the 2018 taxable year. The new proposed regulations also add an extra degree of complexity that must be considered when assessing the guidance for immediate and long-term impact. General background on the GILTI regime, the aforementioned issues and other select highlights from the final and proposed regulations are summarized below.

Background – Section 951A

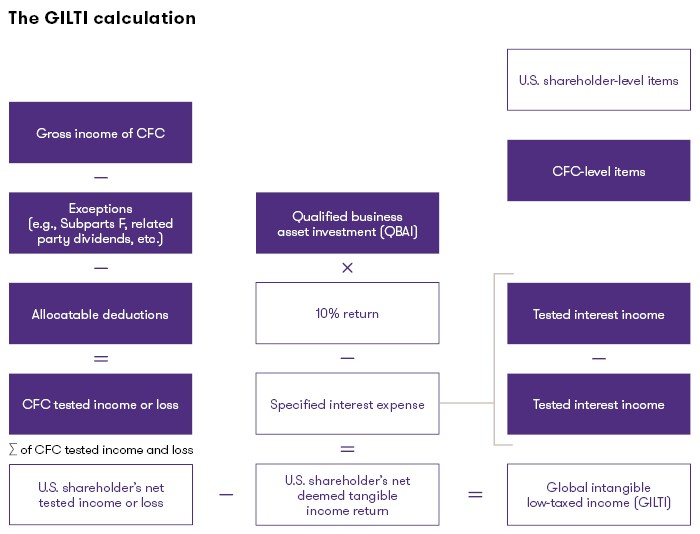

For tax years beginning after 2017, U.S. shareholders of a CFC are subject to current U.S. tax on its GILTI inclusion. GILTI is generally defined as the excess of a U.S. shareholder’s aggregated “net tested income” from CFCs over a routine return on certain qualified tangible assets. This aggregated approach allows loss entities to offset other entities with tested income within the group, but not below zero.

Tested income is the excess, if any, of the corporation’s gross income over its allocable deductions. Certain types of gross income are excluded from being classified as tested income including:

- Income taxed as effectively connected with a U.S. trade or business

- Subpart F income

- Income excluded from foreign-based company income or insurance income by reason of the high-tax exclusion

- Any dividend received from a related person

- Certain foreign oil and gas income

The reduction allowed against tested income for the routine return on tangible assets is defined as 10% of the CFCs’ average aggregate adjusted tax bases in depreciable tangible property, referred to as qualified business asset investment (QBAI), adjusted downward for certain interest expense (collectively, referred to as net deemed tangible income return). The average of the aggregate adjusted tax bases is determined as of the close of each quarter of the taxable year.

The GILTI amount is included in a U.S. shareholder’s income in a similar fashion to Subpart F income. The TCJA provides domestic corporations a 50% deduction of its GILTI amount (37.5% for tax years beginning after 2025), resulting in an effective tax rate on GILTI of 10.5% (13.125% for tax years beginning after 2025), subject to a number of complicating factors.

In September 2018, the IRS released proposed GILTI regulations (REG-104390-18), which provided the general mechanics and structure of the GILTI calculation.

The final regulations

As noted, the final regulations generally retain the approach and structure of the proposed regulations, but with numerous modifications to the general mechanics. Select highlights of these modifications are below.

Pro rata share rules

Several modifications were made with respect to “pro rata share” rules used to determine amounts included in gross income of U.S. shareholders. The proposed regulations provide that a U.S. shareholder’s pro rata share of QBAI is proportional to the U.S. shareholder’s pro rata share of the CFC’s tested income. However, the proposed regulations provided that this rule was subject to an “excess QBAI rule.” The excess QBAI rule required that, to the extent the amount of a tested income CFC’s QBAI is greater than 10 times its tested income for the year, the excess QBAI is allocated solely to common shares (and not to preferred shares). The final regulations generally adopted the QBAI allocation rule included in the proposed regulations, but with modifications to the excess QBAI rule. The final regulations do not limit the excess QBAI rule to preferred stock. Instead, in the case of a tested-income CFC with tested income that is less than 10% of its QBAI, a shareholder’s pro rata share of QBAI is determined based on the shareholder’s pro rata share of the “hypothetical tangible return,” which is defined as 10% of the qualified business asset investment of the tested-income CFC for the CFC inclusion year.

The proposed regulations provided a broad anti-abuse rule that would disregard any transaction or arrangement that is part of a plan, a principal purpose of which is the avoidance of federal income taxation. Commenters to the proposed regulations expressed a number of concerns regarding the scope of this rule and noted that it could be interpreted to apply to nearly all transactions. As a result, the final regulations narrowed the scope to apply only to require appropriate adjustments to the allocation of “allocable E&P” that would be distributed in a hypothetical distribution with respect to any share outstanding as of the hypothetical distribution date.

Rules coordinating Subpart F and GILTI remiges

The final regulations adopted the proposed regulations’ approach to the GILTI high-tax exclusion. Under this approach, a taxpayer may not exclude any item of income from gross tested income under Section 951A(c)(2)(A)(i)(III) unless the income would be foreign base company income or insurance income but for the application of Section 954(b)(4). However, the discussion below details a proposed rule that would expand the scope of the GILTI high-tax exclusion.

The Code generally provides that gross tested income is determined without regard to any gross income taken into account in determining the Subpart F income of the corporation, referred to as the “Subpart F exclusion” in the regulations. When computing Subpart F income, the Section 954(b)(3)(A) de minimis rule provides that if the sum of gross foreign base company income and gross insurance income for the taxable year is less than the lesser of 5% of gross income or $1 million then no part of the gross income for the taxable year is treated as FBCI or insurance income. Alternatively, Section 954(b)(3)(B) full inclusion rule provides that if the sum of gross FBCI and gross insurance income for the taxable year exceeds 70% of gross income, the entire gross income for the taxable year is treated as gross FBCI or gross insurance income, as appropriate. For purposes of the Subpart F exclusion, the final regulations clarify that, subject to the Section 952(c) coordination rule discussed below, gross income taken into account in determining Subpart F income does not include any item of gross income excluded under the de minimis rule or the GILTI high-tax exclusion rule, but generally does include any item of gross income included under the full inclusion rule.

The proposed regulations also provided a coordination rule where gross tested income and allowable deductions properly allocable to gross tested income are determined without regard to the application of Section 952(c) (i.e., the current year E&P limitation). The final regulations generally adopted the rule in the proposed regulations, but revised it to also apply to disregard the effect of a qualified deficit or a chain deficit in determining gross tested income (i.e., the rule prevents a qualified deficit from reducing both Subpart F and tested income).

Specified interest expense

The Code requires a reduction in net deemed tangible income return for interest expense that reduces tested income (or increases tested loss) to the extent the interest income attributable to such expense is not taken into account in determining such shareholder’s net CFC-tested income. The proposed regulations adopted a favorable “netting approach” to determine the amount of interest expense of a U.S. shareholder that is eligible to reduce its pro rata share of tested income. The proposed regulations incorporated a new term, “specified interest expense,” which was defined as the excess of a shareholder’s pro rata share of “tested interest expense” of each CFC over its pro rata share of tested interest income of each CFC. The proposed regulations also provide that regardless of whether interest expense is generated by a tested loss CFC or a tested income CFC, the interest expense is taken into account in determining whether such amounts reduce net deemed tangible income return.

The final regulations generally adopt this netting methodology with certain modifications. First, the final regulations clarify that the definitions of “interest expense” and “interest income” in Section 951A should be defined by reference to “business interest” and “business interest income” in Section 163(j). The final regulations also provide relief to taxpayers by reducing a tested loss CFC’s tested interest expense by an amount equal to 10% of the QBAI that the tested loss CFC would have had if it were instead a tested income CFC.

Accounting methods and QBAI

For purposes of computing QBAI of a CFC, the proposed regulations defined specified tangible property as tangible property used in the production of tested income for which the depreciation deduction provided by Section 167(a) is eligible to be determined under Section 168. The final regulations revise that definition to specifically exclude intangible property that may be eligible for depreciation under Section 168(k), including computer software. Further, the IRS has clarified that in the case of an asset that is partially depreciable (e.g., platinum used in a catalyst) only the portion of the basis that is depreciable is taken into account in computing QBAI.

In determining adjusted basis of specified tangible property for purposes of QBAI, a CFC is required to use the alternative depreciation system (ADS) under Section 168(g) to compute depreciation and to allocate such depreciation deduction of the property ratably to each day in the taxable year. A CFC is also generally required to use ADS in computing income and E&P. However, a non-ADS depreciation method may have been used in prior years when the difference between ADS and the non-ADS depreciation method was immaterial. In order to reduce the potential burden of recalculating depreciation for all specified tangible property that was placed in service prior to the enactment of GILTI, the IRS has provided a transition election to allow use of the non-ADS depreciation method for all property placed in service prior to the first taxable year beginning after Dec. 22, 2017. To qualify for the election, a CFC must not have been required to use, nor actually used, ADS when determining income or E&P, and the election does not apply to property placed in service after the applicable date. The preamble specifically notes that this transition rule does not apply to computations of QBAI for under the foreign-derived intangible income rules.

Grant Thornton Insight:

Although use of this election may be a simplification for taxpayers, it may not produce the best tax result. Taxpayers should analyze the net effect of using ADS or the non-ADS depreciation method before deciding which to use. Making the election also does not impact assets being added generally in 2018, so taxpayers making the election will have both ADS and non-ADS assets when determining QBAI.

In the preamble to the final regulations, the IRS confirms that the determination of the adjusted basis for purposes of QBAI is not a method of accounting. Therefore, a method change under Section 446(e) is neither permitted nor required for a CFC to use ADS for purposes of computing its QBAI. However, the IRS expects that many CFCs may change to ADS for purposes of computing tested income. Such a change is considered a change in method of accounting and a Form 3115, including a Section 481(a) adjustment is required. The change is generally subject to automatic consent under Rev. Proc. 2015-13. The IRS also intends to publish a revenue procedure to update Sections 7.07 and 7.09 of Rev. Proc. 2015-13 to revise the terms and conditions applicable to foreign company method changes (e.g., the separate limitation classification and character of section 481(a) adjustments) to take into account GILTI.

Application to partnerships

The proposed regulations provided a so called “hybrid approach” to partnerships. Under the proposed hybrid approach, a domestic partnership is treated as an entity with respect to partners that are not U.S. shareholders (i.e., indirectly own less than 10% interest in a partnership CFC), but as an aggregate of its partners with respect to partners that are U.S. shareholders (i.e., indirectly own at least 10% in a partnership CFC). While the hybrid approach did strike a balance between the treatment of domestic partnerships and their partners across all provisions of the GILTI regime, it was widely criticized as unduly complex and impractical to administer due to disparate treatment among partners.

The IRS ultimately decided not to adopt the proposed hybrid approach in the final regulations, opting for an aggregate approach. Under this approach, a domestic partnership is treated as an aggregate for purposes of determining the level at which a GILTI inclusion amount is calculated and taken into gross income (irrespective of a particular partners ownership in a partnership CFC). Specifically, for purposes of Section 951A, the Section 951A regulations and any other provision that applies by reference to Section 951A or the Section 951A regulations (e.g., sections 959, 960, and 961), a domestic partnership is generally not treated as owning stock of a foreign corporation within the meaning of Section 958(a). Instead, the partners of a domestic partnership are treated as owning proportionately the stock of CFCs owned by the partnership in the same manner as if the partnership were a foreign partnership under Section 958(a)(2). As a result, the domestic partners, not the domestic partnership, pick-up the GILTI inclusion. However, for purposes of determining U.S. shareholder status, CFC status and whether a U.S. shareholder is a “controlling domestic shareholder” for purposes of making certain elections, a domestic partnership is not treated as foreign partnership. The aggregate approach also applies to S corporations and their shareholders, which are treated as partnerships and partners for purposes of Section 951 through Section 965.

The aggregate rule does not affect the determination of ownership under Section 958(a) for any other provision of the Code (e.g., Subpart F). However, the concurrently issued proposed regulations would extend this treatment to other areas of the Code. See below for further discussion on the proposed regulations.

Anti-abuse rules

The proposed regulations included a rule that generally disallowed, for purposes of calculating tested income or tested loss, any deduction or loss attributable to disqualified basis in depreciable or amortizable property resulting from a “disqualified transfer” of the property. A “disqualified transfer” is a transfer of property from a transferor CFC to a related person during the period that begins Jan. 1, 2018, and ends as of the close of the transferor CFC’s last taxable year that is not a CFC inclusion year.

The final regulations make a number of modifications to the disqualified transfer rule. The scope of rule in the final regulation now applies to deductions or losses attributable to disqualified basis in any property, other than property described in Section 1221(a)(1), regardless of whether the property is of a type with respect to which a deduction is allowable under Sections 167 or 197. Clarification was also provided with respect to the effect of disqualified basis on determining a CFC’s income or gain on the disposition of such property. The final regulations provide that the rule only applies for purposes of determining whether a deduction or loss is properly allocable to gross tested income, Subpart F income, or effectively connected income. Therefore, disqualified basis is not considered when computing income or gain on the disposal of such property. By allocating a deduction or loss to residual CFC gross income, the rule in the final regulations ensures that any deduction or loss attributable to disqualified basis is also not taken into account for purposes of determining the CFC’s Subpart F income or effectively connected income.

The proposed regulations also contained a per se anti-abuse rule that disregarded certain temporarily held specified tangible property when computing QBAI. The final regulations clarify that the rule would apply only if, in the absence of the rule, the holding of property would increase the deemed tangible income return of an applicable U.S. shareholder. The final regulations also include a safe harbor involving transfers between CFCs that is intended to exempt non-tax motivated transfers from anti-abuse rules. Additionally, a CFC’s holding period under the rule does not include any tacked holding periods from other persons. Most importantly, the 12-month per se rule is modified to be a presumption that may be rebutted by attaching a statement to the Form 5471 that must explain the specific facts and circumstances supporting the rebuttal. This is welcome relief for taxpayers that may have transactions with substantial non-tax purposes that may otherwise have run afoul of the rule in the proposed regulations.

Basis adjustment for ‘used-tested loss’

The proposed regulations required a U.S. corporate shareholder to reduce its tax basis in the stock of a tested loss CFC by the “used-tested loss” for purposes of determining gain or loss upon disposition of the tested loss CFC. Due to significant comments raised with respect to this rule, the final regulations reserve on rules related to basis adjustments of tested loss CFCs.

Foreign tax credit regulations

In addition to the GILTI regulations discussed above, the package also contained final regulations under Sections 78 and 965 and final and temporary regulations under Section 861. These rules were all previously proposed in the broader foreign tax credit package released last November. The final regulations:

- Finalize a proposed rule (without modification) that provides that a dividend under Section 78 that relates to the taxable year of a foreign corporation beginning prior to Jan. 1, 2018, should not be treated as a dividend for purposes of Section 245A.

- Finalize proposed ordering rules (with some modifications) addressing the application of Section 965(n) (i.e., election to forgo the use of net operating losses in determining the Section 965 amount).

- Finalize proposed regulations under Section 861 (with some modifications) that clarifies certain rules for adjusting the stock basis in a 10%-owned corporation, including that the adjustment to basis for E&P includes previously taxed earnings and profits.

These rules have special applicability dates. A special applicability date is provided in Treas. Reg. Sec. 1.78-1(c) in order to apply the second sentence of Tres. Reg. Sec. 1.78-1(a) to Section 78 dividends received after Dec. 31, 2017, with respect to a taxable year of a foreign corporation beginning before Jan. 1, 2018. The Section 965 rules contained in this final regulation apply beginning the last taxable year of a foreign corporation that begins before Jan. 1, 2018, and with respect to a United States person, beginning the taxable year in which or with which such taxable year of the foreign corporation ends. Finally, the rules for adjusting the stock basis in a 10% owned corporation under Section 861 are generally applicable to taxable years that both begin after Dec. 31, 2017 and end on or after Dec. 4, 2018, (Treas. Reg. Secs. 1.861-12 (c)(2)(i)(A) and (B)(1)(ii) also apply to the last taxable year of a foreign corporation that begins before Jan. 1, 2018, and with respect to a United States person, the taxable year in which or with which such taxable year of the foreign corporation ends).

GILTI applicability dates

Consistent with the applicability date of Section 951A, Treas. Reg. Secs. 1.951A-1 through 1.951A-6 apply to taxable years of foreign corporations beginning after Dec. 31, 2017, and to taxable years of U.S. shareholders in which or with which such taxable years of foreign corporations end.

The proposed regulations

High-tax exclusion

Section 951A(c)(2)(A)(i)(III) provides that any gross income excluded from the foreign base company income and the insurance income of a CFC by reason of Section 954(b)(4) is not treated as gross tested income. This is referred to in the regulations as the “GILTI high-tax exclusion.” Section 954(b)(4) provides that foreign base company income and insurance income shall not include any item of income received by CFC if the taxpayer establishes that such income was subject to an effective rate of income tax imposed by a foreign country greater than 90% of the maximum rate of tax specified in Section 11 (i.e., 21% or the maximum corporate rate).

As discussed above, the final regulations adopted the proposed regulations approach to the GILTI high-tax exclusion. Under this approach, a taxpayer may not exclude any item of income from gross tested income under Section 951A(c)(2)(A)(i)(III) unless the income would be foreign base company income or insurance income but for the application of Section 954(b)(4).

The application and scope of the GILTI high-tax exclusion has been widely debated in the press and in comment letters. In response to these comments, the IRS proposed that the GILTI high-tax exclusion be expanded to include certain high-taxed income even if that income would not otherwise be foreign base company income or insurance income. Under the proposed regulations, the GILTI high-tax exclusion would be made on an elective basis. In essence, the proposed election would allow CFCs to exclude gross income from tested income that is subject to a “high” effective rate of tax. The effective tax rate test is 90% of the maximum effective rate (or 18.9%), and is determined based on the amount that would be deemed paid under Section 960 if the item of income was Subpart F. The effective rate test would be performed at the qualified business unit level.

If the election is made, it also applies with respect to each item of income that meets the effective rate test of each CFC in a group of commonly controlled CFCs. In other words, it cannot be made selectively, or only with respect to certain CFCs. The election applies for current and future years unless revoked. Although it can be revoked, the election is subject to a 60-month lock-out period where the election cannot be re-elected if it has been revoked (as well as a similar 60-month lock-out if it is made again after the first 60-month period). This 60-month rule is subject to an exception for changes in control. The proposed GILTI high-tax exclusion cannot be relied upon until the regulations are issued as final.

Grant Thornton Insight:

In many cases, the proposed GILTI high-tax exclusion could provide much needed relief for certain taxpayers. However, as drafted, the election is not one-size-fits-all. The election could produce unfavorable results for certain taxpayers. For example, if a taxpayer has a high-taxed CFC and a low-taxed CFC, the election would exclude from tested income the income of the high-taxed CFC, but not the income of the low-taxed CFC. The high-taxed CFC’s income would have otherwise carried credits that could have shielded some or all of the low-taxed CFC’s income from incremental U.S. tax.

Application to partnerships

The proposed regulations would apply an aggregate approach to domestic partnerships. Specifically, the proposed regulations provide that, for purposes of Sections 951, 951A and any provision that applies by reference to Sections 951 and 951A, a domestic partnership is not treated as owning stock of a foreign corporation within the meaning of Section 958(a). Rather, a domestic partnership is treated in the same manner as a foreign partnership. This rule does not apply, however, for purposes of determining whether any U.S. person is a U.S. shareholder, whether a U.S. shareholder is a controlling domestic shareholder, as defined in Treas. Reg. Sec. 1.964-1(c)(5), or whether a foreign corporation is a CFC.

Similar to the rule described above in the final regulations, a domestic partnership that owns a foreign corporation is treated as an entity for purposes of determining whether the partnership and its partners are U.S. shareholders, whether the partnership is a controlling domestic shareholder, and whether the foreign corporation is a CFC. However, the partnership is treated as an aggregate of its partners for purposes of determining whether (and to what extent) its partners have inclusions under Sections 951 and 951A and for purposes of any other provision that applies by reference to Sections 951 and 951A. This aggregate treatment does not apply for any other purposes of the Code, including Section 1248.

Grant Thornton Insight:

Application of this rule could eliminate Subpart F inclusions (as well as GILTI inclusions, which is already the case under the final regulations) for shareholders that own less than 10% in a CFC indirectly through a domestic partnership. The regulations contain an example illustrating this point. In the example, a U.S. individual owns 5% and a domestic corporation owns 95% in a domestic partnership that in turn that owns 100% of a CFC. Because the individual indirectly owns less than 10% in the CFC, the individual is not a United States shareholder and thus does not have an income inclusions under Section 951 or a pro rata share of any amount for purposes of Section 951A. Domestic partnerships, particularly those with diverse ownership, should carefully review these provisions and assess the potential impact of early adopting these rules.

Applicability dates

The changes related to the GILTI high-tax exclusion election are proposed to apply to taxable years of foreign corporations beginning on or after the date that final regulations are published, and to taxable years of U.S. shareholders in which or with which such taxable years of foreign corporations end. As a result, the regulations would not be effective until at least 2020 for calendar-year taxpayers.

The proposed rules addressing the treatment of domestic partnerships as foreign partnerships are proposed to apply to taxable years of foreign corporations beginning on or after the date of publication, and to taxable years of a U.S. person in which or with which such taxable years of foreign corporations end. However, a domestic partnership may rely on the rules for tax years of a foreign corporation beginning after Dec. 31, 2017, and for tax years of a domestic partnership in which or with which such tax years of the foreign corporation end (subject to a related party consistency rule).

Next steps

The final GILTI regulations generally retain the approach and structure of the proposed regulations, but there are a number of significant departures from the proposed rules. Many of the final rules apply retroactively to 2018. Inevitably, this means many taxpayers must now revisit and revise any completed GILTI calculations, and consider the final rules when preparing 2018 tax returns. Further, taxpayers who have already filed 2018 tax returns with GILTI inclusions must consider whether amended returns should be filed.

The retroactive applicability date also carries financial statement implications. A company with a reporting period (annual or interim) ending after June 14 will need to evaluate whether the regulations constitute new information which causes a change in judgment with respect to the recognition and measurement of unrecognized tax benefits for financial statement purposes.

Even with concrete rules provided in the final package, the simultaneous release of the proposed GILTI high-tax exclusion leaves taxpayers uncertain about the future state of GILTI. The GILTI high-tax exclusion would require taxpayers to completely rethink the GILTI calculus, and also usher in new planning opportunities. If finalized, it could offer significant relief to certain taxpayers, but not without its own risks. Given its proposed state, taxpayers should carefully assess the impact of GILTI, both with and without the GILTI high-tax exclusion, on their specific tax circumstances.

Contacts:

Tax professional standards statement

This content supports Grant Thornton LLP’s marketing of professional services and is not written tax advice directed at the particular facts and circumstances of any person. If you are interested in the topics presented herein, we encourage you to contact us or an independent tax professional to discuss their potential application to your particular situation. Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein. To the extent this content may be considered to contain written tax advice, any written advice contained in, forwarded with or attached to this content is not intended by Grant Thornton LLP to be used, and cannot be used, by any person for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

The information contained herein is general in nature and is based on authorities that are subject to change. It is not, and should not be construed as, accounting, legal or tax advice provided by Grant Thornton LLP to the reader. This material may not be applicable to, or suitable for, the reader’s specific circumstances or needs and may require consideration of tax and nontax factors not described herein. Contact Grant Thornton LLP or other tax professionals prior to taking any action based upon this information. Changes in tax laws or other factors could affect, on a prospective or retroactive basis, the information contained herein; Grant Thornton LLP assumes no obligation to inform the reader of any such changes. All references to “§,” “Sec.,” or “§” refer to the Internal Revenue Code of 1986, as amended.

More flash

No Results Found. Please search again using different keywords and/or filters.